The COVID-19 global pandemic is a public health crisis of unprecedented proportions that has upended the global economy in ways we’re only beginning to understand. On March 27th, 2020 the CARES Act legislation was enacted, which included critical relief for single family residential homeowners with federally-backed mortgage loans.[1] Among other relief, the CARES Act created a 60-day foreclosure moratorium, as well as the right for borrowers to request forbearance (i.e., a pause) to their mortgage payments for an initial term of up to 180 days, with the right to request an extension for up to an additional 180 days.

Over the last month, mortgage market stakeholders and policymakers alike have worked hard to put this important legislation into practice. Among the early operational concerns to emerge, which continues to be a topic of discussion, is the possible risk of financial disruption to mortgage servicers that own the mortgage servicing rights (MSR) to the mortgage loan.[2] When borrowers initiate a pause to their monthly payments, it’s their servicer that ensures mortgage principal and interest continues to be “advanced” to the bond investor, along with escrowed property taxes to the county and escrowed homeowners insurance to the insurance carrier (these payment components are referred to as “PITI”).[3]

Importantly, when mortgage servicers advance PITI payments on behalf of the borrower, they source the capital from their own balance sheet, typically in the form of a line of credit they hold with another financial institution or even with their own cash reserves. However, this outlay is intended to be short-term; after varying periods of time, the servicer is reimbursed for these advances by the applicable federally-backed mortgage program.[4]

Under ordinary circumstances, this system continues uninterrupted. However, when unexpected catastrophes occur on a significant scale, as is the case with the COVID-19 national emergency, mortgage servicer liabilities have the potential to outstrip available assets of at least some servicers. This is a particular risk for non-bank servicers that tend to hold less capital relative to their bank servicer counterparts that have retail deposit bases to draw from.

Accordingly, policymakers and regulators have been closely monitoring the number of homeowners that request their right to forbear their mortgage payments. They are also monitoring the impacts of servicer advance requirements on the health of servicer balance sheets; particularly given the significant demands on servicer capital. Based on this ongoing monitoring effort, regulatory agencies overseeing the federally-backed mortgage programs have announced a series of program and policy changes that provide liquidity relief to servicers, which industry has welcomed. These actions may well ensure sufficient liquidity relative to both PI and TI advances, however, discussions persist in some quarters with respect to whether more needs to be done to ensure servicers have the ability to advance escrowed property tax payments and homeowners insurance premiums in a timely fashion. The implications of a material drop off in escrowed TI advances extends beyond mortgage market and homebuyer disruptions. Municipalities tend to rely, at least in part, on timely receipt of property tax revenues (whether advanced by the servicer via escrow account disbursement or paid directly by the borrower) to fund their basic services and public works.[5]

Accordingly, the objective of this spotlight series is to make available data and facts that can assist regulators and industry stakeholders alike as they evaluate possible risks of a material drop-off in servicer advances of escrowed property tax payments or delinquent non-escrow borrower property tax payments. As the largest provider of property tax and escrow services to the single family residential mortgage markets, CoreLogic is uniquely positioned to size the universe of escrowed property tax payments expected to be advanced by servicers over the course of the remainder of 2020, including what the outer-boundary of potential risk exposure to municipalities may look like at varying levels of forbearance activity, among other insights.

Sizing the Overall Market for Municipal Property Tax Payments

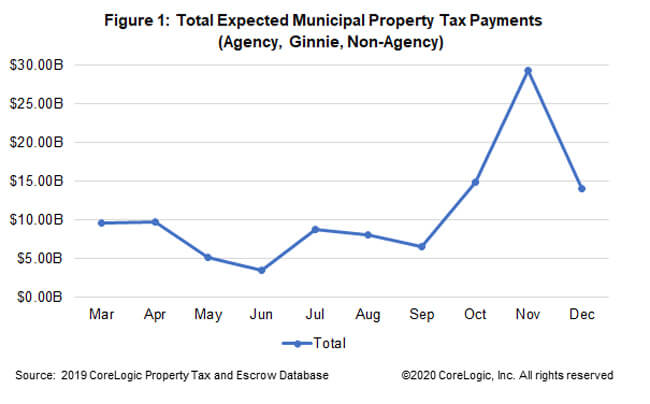

We begin by forecasting the universe of property tax payments expected by county tax collectors from March through December of 2020.[6] Figure 1 includes all expected property tax payments where the homeowner holds a single family residential mortgage loan, inclusive of both escrow account borrowers whose payments are advanced by their servicer, as well as borrowers who have received an escrow waiver from their servicer and make their payments directly to the county. Expected property tax revenues for homeowners that own their homes free and clear (i.e., no mortgage loan) are not included in these figures.

Figure 1 displays a range of roughly $4B-10B in expected monthly tax payments from March through September, before spiking to $14.95B in October, peaking at $29.35B in November, and ending the year at $14.04B in December. To the extent COVID-19 forbearance requests are less frequent and shorter-term in their duration, it would represent a relative tailwind for municipalities. This is particularly true for municipalities that are not scheduled to receive the bulk of their property tax payments in the initial months of COVID-19’s economic impact, offering them precious time to prepare for any potential disruption to cash flow.

When sizing municipal property tax payments at risk of disruption stemming from COVID-19 forbearance requests, it is important to recognize is that the CARES Act right to forbearance only applies to principal and interest payments for federally-backed loan programs. It does not provide borrowers with a right to forbear their property tax and insurance payments. With that said, given that borrowers are accustomed to paying a single monthly mortgage payment that is composed of PITI, it will be important to keep a close eye on whether borrowers are aware of these facts (or are often confused about the difference between PI and TI payments relative to forbearance) and, regardless, are demonstrating the ability and/or willingness to continue to make TI payments to their servicer.

Sizing the Portion of Bank and Non-Bank Servicer Escrow Advances

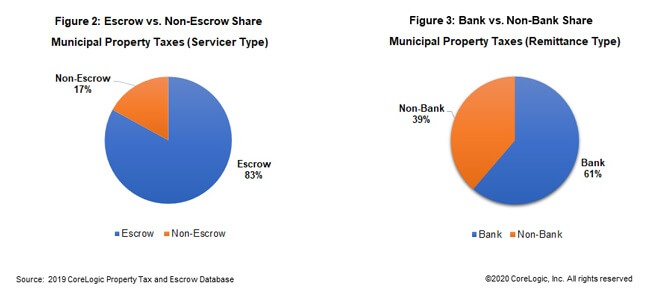

So that we may better account for the different types of potential disruptions to the flow of expected property tax payments, Figures 2 and 3 segment the population of payments originating from borrower escrow accounts advanced by bank and non-bank servicers, respectively.

Figure 2 demonstrates that 83% of expected property tax payments will be made through escrow accounts maintained by the servicer, while 17% of property tax payments will be made directly by borrowers who receive escrow account waivers from their servicer. Figure 3 demonstrates that 61% of expected escrowed property tax payments will be advanced by bank servicers, while 39% will be advanced by non-bank servicers. This information assists us with breaking down the universe of expected property tax payments that could be impacted by delays stemming from either potential servicer liquidity disruptions or delinquent borrower-direct payments (in the case of non-escrow account borrowers) due to COVID-19 borrower forbearance requests.

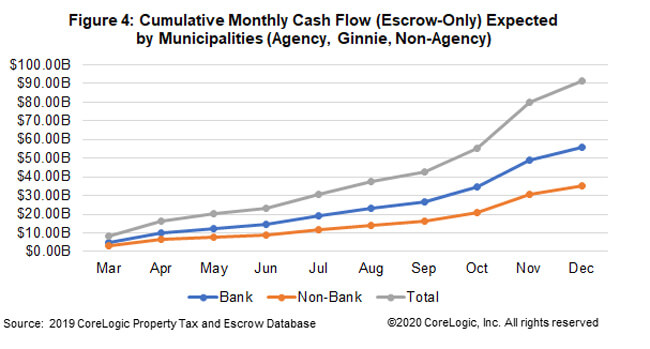

Taking the above segmentation data into account, Figure 4 displays the cumulative expected monthly cash flow expected by municipalities from March through December of 2020, stemming from servicer escrow account disbursements and broken down by bank and non-bank servicers.

Figure 4 demonstrates that the cumulative monthly cash flows expected from non-bank servicer escrow account disbursements builds from $3.39B in March, reaching double-digits ($11.56B) in July, and capping out at $35.39B in December. With respect to bank servicer escrow account disbursements, they also build from $4.63B in March, reaching double-digits ($12.56B) earlier in May, and capping out at $55.96B in December. In total, cumulative monthly cash flows from servicer escrow account disbursements is forecast to be $91.36B for the period of March to December of this year.

Determining the Possible Forborne Portions of Bank and Non-Bank Servicer Escrow Advances

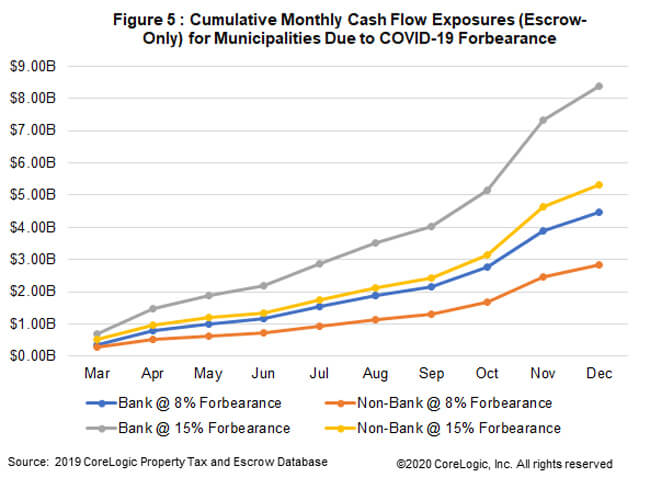

Next, merely as a means of sizing the portion of cumulative monthly cash flows that may be at some risk of disruption as a result of any material dislocations in some sectors of the mortgage servicing market, Figure 5 applies a simple factor to further subset this population based upon potential borrower forbearance activity.

Figure 5 displays the universe of possible forborne cumulative monthly property tax payments, some subset of which could become delinquent, depending on how many borrowers ultimately request their right to forbearance, how effectively the borrower is able to recover based on the post-forbearance loss mitigation option offered to them, and, also the ability of the servicer to maintain sufficient capital to fulfill their advance obligations or for the MSRs to have been successfully transferred to another servicer which can. As of April 19, the Mortgage Bankers Association (MBA) reports that 6.99% of mortgage borrowers have requested forbearance.[7] Included in Figure 5 is a projection of cumulative forborne property tax payments, assuming an optimistic case of 8% and a pessimistic case of 15%.

Based on the optimistic case (8% forbearance), total forborne non-bank servicer advances cross the $1B threshold in August, with total forborne advances of $2.83B. Forborne bank servicer advances cross the $1B threshold in May, with total forborne advances of $4.48B.

Based on the pessimistic case (15% forbearance), forborne non-bank servicer advances cross the $1B threshold in May, with total forborne advances of $5.31B. Forborne bank servicer advances cross the $1B threshold in April, with total forborne advances of $8.39B.

It is important to reiterate that these data do not attempt to forecast the cash flows that are expected to actually become delinquent or to project the extent of the effect of a temporary drop off in revenues due to any potential servicer advance disruptions. Rather, they represent possible outer boundaries of forborne monthly property tax payments that have the potential to become delinquent. Potential drivers of delinquency include deterioration of a servicer’s available capital and/or inability to raise fresh capital or tap available credit lines (some servicers will be more resilient than others). In the event a servicer is no longer able to fulfill their advance obligation, the federally-backed mortgage program must transfer the MSRs to another mortgage servicers willing to take on the obligations. Other potential drivers of delinquency might also include borrowers that are unable to sustain their monthly mortgage payments, including their property tax payments, once they exit forbearance and/or enter into a loss mitigation workout option, particularly in the case of non-escrow account borrowers who make their payments directly to the county.

Conclusion

With the financial stress to homeowners mounting, some of the top 20 (and many other) MSAs/Counties are already making contingency plans. For example, while Los Angeles County has not extended their ELD for property tax payments, they have announced that delinquent taxpayers can apply for a workout plan for any missed payments. Philadelphia County has moved their ELD to July to give taxpayers extra time to make their payments (i.e., forbearance for property tax bills). Likewise, King County (Seattle) has extended the deadline for non-escrow account borrowers from April to June. Finally, San Francisco County has moved their ELD to May to provide their taxpayers some relief. We expect this type of property tax loss mitigation to expand over the coming weeks. These mitigation efforts suggest that MSAs/counties are aware of the risk of a drop off in property tax revenue.

Over time we will be able to measure actual material impacts (if any) to municipal property tax payments stemming from possible disruptions or delays by financially stressed mortgage servicers or delinquent non-escrow account mortgage borrowers. Regulators will continue to monitor mortgage servicers’ ability to fulfill their obligations to advance property tax payments that are a source of revenue for municipalities.

[1] Includes loan programs offered by Fannie Mae, Freddie Mac, and Ginnie Mae (including FHA, VA, and USDA programs)

[2] Also known as “mortgage lenders,” the mortgage servicer is the company to whom borrowers sends their monthly mortgage payment

[3] The federally-backed mortgage lending programs require servicers to establish borrower escrow accounts to help ensure the borrower’s timely payment of property taxes, homeowners insurance, and any other applicable assessments on their property, in addition to the borrower’s monthly principal and interest payments on the mortgage loan. Note that Fannie Mae and Freddie Mac permit servicers to waive the escrow account requirement for borrowers under certain circumstances, which are the relative exception. The analysis herein distinguishes between servicer advances of property taxes from the borrower’s escrow account and non-escrowed property tax payments made directly by the borrower.

[4] Each federally-backed mortgage lending program has its own requirements for the PITI components the servicer is expected to advance. For example, Fannie Mae and Freddie Mac requires some servicers to advance ITI-only and others TI only. Fannie Mae requires others still to advance the full PITI, as does Ginnie Mae. Moreover, each program has different event triggers and timeframes defining when servicer advances can cease and receive reimbursement during the COVID-19 national emergency.

[5] Some and perhaps many MSAs/counties have a range of tax revenue sources and some also may have better reserves in place than others. Predicting the consequence to a given MSA/country of even a material drop off in property tax revenues isn’t within the purview of this research.

[6] Note that we use 2019 actual payments as the basis for our March-December 2020 monthly forecast. Actual payment amounts may vary based on property tax changes for 2020 (property tax rate and expected liquidity date), though not by orders of magnitude.

[7] See MBA Forbearance and Call Volume Survey at https://newslink.mba.org/servicing-newslink/2020/april/mba-servicing-newslink-tuesday-april-21-2020/mba-weekly-survey-share-of-mortgage-loans-in-forbearance-rises-to-5-95/

2020 © CoreLogic,Inc. All rights reserved.