Home Price Index Highlights: January 2021

- National home prices increased 10% year over year in January.

- Annual price increases are expected to slow during 2021.

Overall HPI Growth

National home prices increased 10% year over year in January 2021, according to the latest CoreLogic Home Price Index (HPI®) Report. The January 2021 HPI gain was up from the January 2020 gain of 4.1% and was the highest year-over-year gain since November 2013. Low mortgage rates and low for-sale inventory drove the increase in home prices, however affordability constraints may work to slow home price growth later this year.

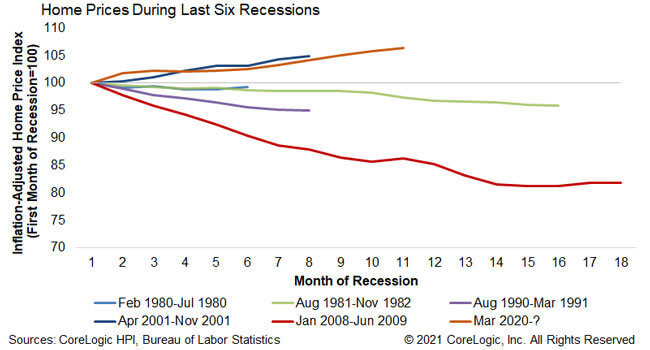

Impact of Recession on Home Prices

The recession that started in March 2020 did not slow home price growth, as has been the case in some previous recessions. Figure 1 shows movements in the inflation-adjusted HPI[1] for the six most recent recessions starting from the first month and through the end of each recession. Numbers below 100 indicate falling home prices, which has been a feature of four of the six recessions. However, at 11 months in, the 2020 recession is following the path of the 2001 recession, which is the only other one of the six with increasing home prices. The worst of the six recessions was the Great Recession that started in 2008, which was characterized by excess supply of homes for sale, which is not the case in today’s tight-supply housing market.

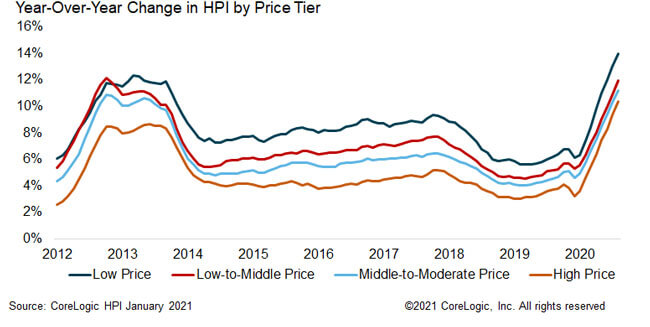

HPI Growth by Price Tier

CoreLogic analyzes four individual home-price tiers that are calculated relative to the median national home sale price[2]. Home price growth accelerated for all four price tiers to the highest rates since 2013 for the low-to-middle and since 2006 for the other three price tiers. The lowest price tier increased 14% year over year in January 2021, compared with 12% for the low- to middle-price tier, 11.2% for the middle- to moderate-price tier, and 10.4% for the high-price tier. Entry-level homes are in high demand by first-time buyers while in short supply, leading to affordability pressures for these buyers.

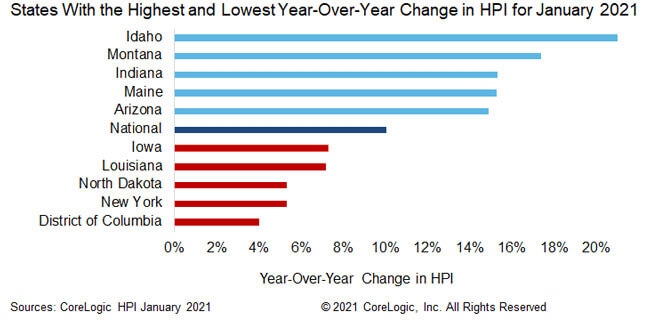

State-Level Results

Figure 3 shows the year-over-year HPI growth in January 2021 for the 5 highest- and lowest-appreciating states. All states showed annual increases in HPI in January, and Idaho led the states in appreciation with appreciation of 21%, double the rate of appreciation from a year earlier. At the low end, Washington, D.C. saw an increase in home prices of 4%. The surge in home price appreciation was felt across the country, with all states showing higher appreciation in January 2021 than in January 2020. Montana and Connecticut had the biggest acceleration in home price growth from January 2020 to January 2021. Connecticut is notable because price growth for this state was near zero in January 2020 but increased to 13.1% in January 2021. This turnaround can be partly attributed to an influx of buyers from metropolitan areas in nearby states.

Home price growth started the new year with double-digit gains and strong gains are expected to persist for much of this year. However, as affordability constrains first-time buyers and for-sale inventory increases, prices gains should slow in late 2021. For more information on home price insights and trends, check out our latest HPI Report.

© 2021 CoreLogic, Inc. All rights reserved

[1] The Consumer Price Index (CPI) Less Shelter was used to create the inflation-adjusted HPI. It is important to adjust the HPI for inflation to compare recessions, especially since two of the recessions occurred during very high inflation periods.

[2] The four price tiers are based on the median sale price and are as follows: homes priced at 75% or less of the median (low price), homes priced between 75% and 100% of the median (low-to-middle price), homes priced between 100% and 125% of the median (middle-to-moderate price) and homes priced greater than 125% of the median (high price).