Unlike the Great Recession, the speedy intervention provided by the CARES Act ensured mortgage forbearance options for homeowners who were financially harmed by the pandemic recession and had a federally backed loan. And while forbearance options will help some homeowners keep their homes, the path of employment rebound – which is still unclear – will be a critical determinant for many delinquency outcomes. Nationally, serious delinquencies (mortgage loans 90+ days past due or in foreclosure) in July reached 4.1%, up from 1.2% recorded prior to the onset of the pandemic.

The following analysis focuses on serious delinquencies in California since the state was one of the epicenters of the foreclosure crisis in the Great Recession and the natural concern remains about how the current crisis will impact the state’s housing market. At its peak in January 2010, the serious delinquency rate reached 11.4% in California, up from 0.3% in 2005 – prior to the onset of the housing crisis. In March 2020, serious delinquencies were at 0.6% and have reached 3.8% by July.

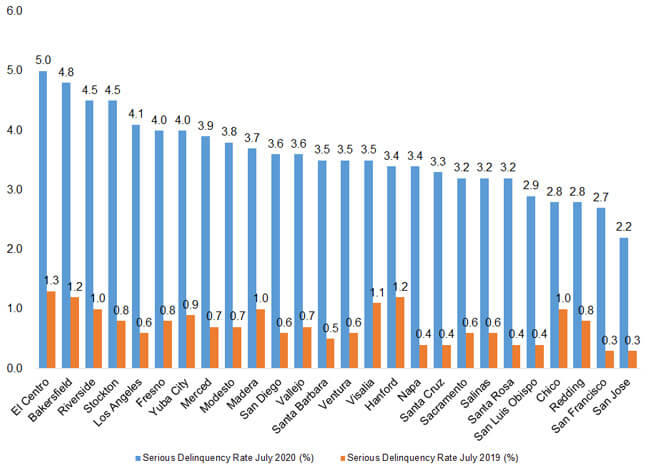

While the serious delinquency rate in July is still only a third of that during the last recession, some metro areas in the state have seen a larger increase in delinquencies. Figure 1 illustrates the serious delinquency rate by metro in July 2020 compared to a year ago. Unfortunately, some of the same areas that struggled in the previous foreclosure crisis are again seeing elevated delinquency rates, particularly areas in the Inland Empire and Central Valley, such as Bakersfield, Riverside and Stockton. El Centro, which reported the highest delinquency rate, is a border town in southeastern California with the second highest unemployment rate in the country even prior to the pandemic. For all reported metros, serious delinquencies have increased about four-fold.

Nevertheless, homeowners faced with delinquency in the current recession have more options than were available in the Great Recession. One, mentioned above, is the forbearance option. In July, 8.6% of loans in California were in forbearance – similar to the national rate of 8.5%. But, almost 40% of those who opted for a forbearance continued to make payments on their mortgages thus not becoming delinquent on their loans. The second option that current homeowners have is the availability of home equity which provides homeowners with liquidity necessary to avoid a foreclosure even if they faced income loss from unemployment. In other words, when faced with loss of income and inability to pay a mortgage, homeowners with home equity can still opt to sell their home and avoid a foreclosure.

Average homeowners’ equity in California in the second quarter of 2020 was over $400,000, compared to the U.S. average of $185,000.

And while not all homeowners have equity, the CoreLogic Home Equity Report found that at mid-year the percent of mortgaged homes with negative equity in California had declined to 1.7%, the lowest since the Great Recession and just a fraction of the ‘underwater’ peak of 37.3% at the end of 2009.

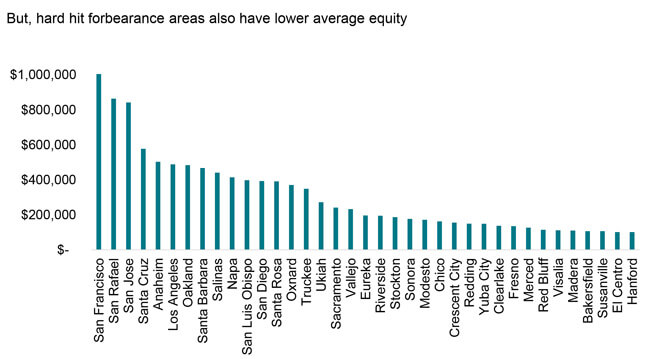

Figure 2 illustrates average homeowner equity across California metro areas. Not surprisingly, greater Bay Area metros top the list with average equity ranging from $600,000 to $1 million, though many of the other regions in Southern California and Central Coast still hover around $500,000. On the other side, the areas with elevated delinquencies have seen slower price growth over the last decade and hence slower accumulation of equity, though the average equity across the Central Valley and Inland Empire is still about $100,000.

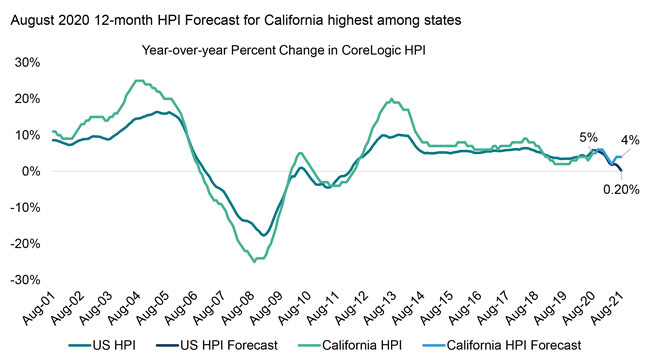

Now, while home prices have generally fallen during previous recessions causing homeowners to lose equity, housing fundamentals specific to the current recession have led to an acceleration of home price growth[1]. And according to the August 2020 CoreLogic Home Price Forecast, home prices in California are expected to continue the annual increase and grow at 4% in August 2021 (Figure 3). Still, most of California’s price growth will be driven by coastal areas, such as San Francisco and San Diego, but according to the CoreLogic Market Risk Indicator, only the Modesto metro area has greater risk (65% or higher) of seeing a price decline through next August.

[1] https://www.corelogic.com/blog/2020/10/home-price-appreciation-accelerates-as-buyers-compete-for-limited-supply-of-homes.aspx