Overnight, Hurricane Sally strengthened to a high-end Category 2 storm, making landfall near Gulf Shores, Alabama with maximum sustained winds of 105mph. Interestingly, Sally made landfall in almost the exact same spot and on the same day, September 16, as Hurricane Ivan in 2004.

Wind

Sally was a moderate sized storm with hurricane-force winds extending up to 40 miles from the center and tropical storm-force winds extending as far out as 125 miles.

Storm Surge

Hurricane Sally trended slightly eastward, producing strong storm surge in Alabama and the western end of the Florida panhandle. Early reports indicate approximately five feet of storm surge flooding in the Pensacola area. The late shift eastward made Pensacola more vulnerable to surge than originally expected 24 hours prior to landfall.

In addition, the relatively slow forward movement of the storm enabled it to push more surge water onto land. This exacerbated the flood potential by combining with the rainfall it is producing. With the hurricane slowly approaching the coast, the rainfall sourced flooding onshore is often prevented from flowing downstream to the Gulf by the surge water that is being pushed ahead of the storm and upstream. The combined effect is increased flood levels inland.

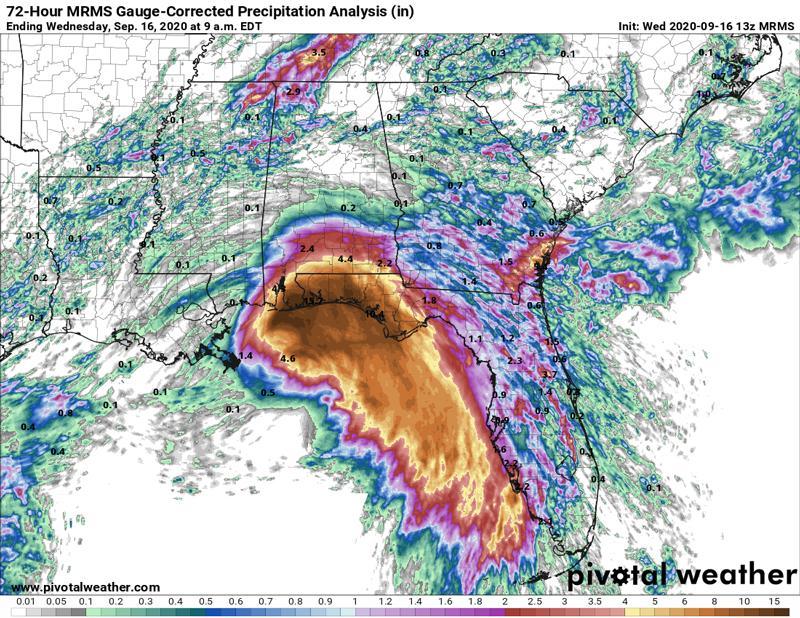

Figure 1

72-Hour MRMS Gauge-Corrected Prescription Analysis

Source: CoreLogic Inc.

© 2020 CoreLogic,Inc., All rights reserved.

Rainfall

Extreme rainfall in excess of 30 inches has been reported along the Gulf Coast, resulting in widespread catastrophic flash flooding with multiple streams having already risen over 15 feet. Flooding is excepted to spread further inland as Sally slowly makes its way through southern Alabama and Georgia.

As of Wednesday afternoon, Sally has weakened and was downgraded to a Tropical Storm. CoreLogic will continue to provide updates as the situation unfolds.

What is the purpose of Hazard HQ and who is it designed for?

Hazard HQ’s purpose is to arm our core audience of insurers, mortgage professionals, and media with information that allows them to make educated decisions that help people most effectively protect their homes, businesses, and families. Here at Hazard HQ™ you’ll find press releases, explanations of how our data works, commentary about what kind of damage we foresee, and critical thinking on what it takes to be more resilient in the face of natural hazards—be it a hurricane, volcano, earthquake, or beyond.

We know data can get confusing and that clarity is important amidst the chaos, so we want to make sure you’re finding all the information you need to be up to date in one place.

- What is reconstruction cost value (RCV)?

CoreLogic uses its RCV methodology which estimates the cost to rebuild the home in the event of a total loss and is not to be confused with property market values or new construction cost estimation. Reconstruction cost estimates more accurately reflect the actual cost of damage or destruction of residential buildings, since they include the cost of materials, equipment and labor needed to rebuild. These estimates also factor in geographical pricing differences (although actual land values are not included in the estimates).

- What is damage?

Damage is the overall sum of money lost, both insured and uninsured.

- What is loss?

Loss, otherwise known as gross loss or ground-up damage, is the insured portion of the damage sum. It is the portion that insurance companies pay out.

- Why are there so many different numbers with every press release?

At CoreLogic, we break down the risk of damage cumulatively. If any hurricane hits, no matter the Category*, it will cause storm surge in the Extreme risk areas. These are homes that typically are closest to the coast and lowest in elevation, thus susceptible to every type of hurricane from Categories 1 to 5. Therefore, their risk of impact is Extreme.

Similarly, the strongest Category 5 hurricane will cause storm surge induced flooding furthest inland. It is listed in the table as Low risk because these hurricanes are the least likely to incur damage, not because they do less damage. However, because a Category 5 hurricane will also cause damage at more vulnerable properties, the cumulative amount of homes affected and the total RCV both increase. These hurricanes affect the same areas that weaker hurricanes do and more.

*Categories are measured on the Saffir-Simpson Hurricane Wind Scale (SSHWS).

- Why can’t you deliver an estimate of rainfall induced flooding sooner?

In order to develop an estimate about the rainfall, we first need a footprint of where we think the rain is going to fall. Once the storm is conclusive, we can better understand where it’s going to make landfall and predict where that path will take it.

- Why can’t you provide more specific insight to underinsured/uninsured properties impacted?

Underinsurance is difficult to measure and report on. The market – and climate – are constantly changing and with that, risk changes. CoreLogic recommends ongoing conversations with your realtor and insurer to determine your own level of protection.

- Why don’t you put out insights for every event? What constitutes as “substantial”?

CoreLogic takes many factors into consideration when deciding to share insights including but not limited to: number of casualties, number of properties damaged, reconstruction cost value, and frequency of events. If you are in need of insights not listed on HHQ, please feel free to reach out for more information.

- Can you share a YoY comparison for homes at-risk?

CoreLogic advises against comparing homes at-risk year over year. This is because there are many factors that go into the risk score of a region’s homes – previous fire activity, new construction, changing vegetation, short-term weather patterns, etc. While the totals might change YOY, this doesn’t indicate an apples-to-apples comparison.

- What can you tell us about the meteorology behind any natural hazard?

What we can provide is a realistic assessment of how a catastrophe impacts people—their homes and businesses—and what that will look like, both insured and uninsured. We are able to do this with both our highly granular catastrophe models to determine the impact upon properties and with a team of Ph.D.-level scientists who work hard to Get The Whole Story.

- Who should I reach out to with media questions or more information?

You can reach out to [email protected] or [email protected].