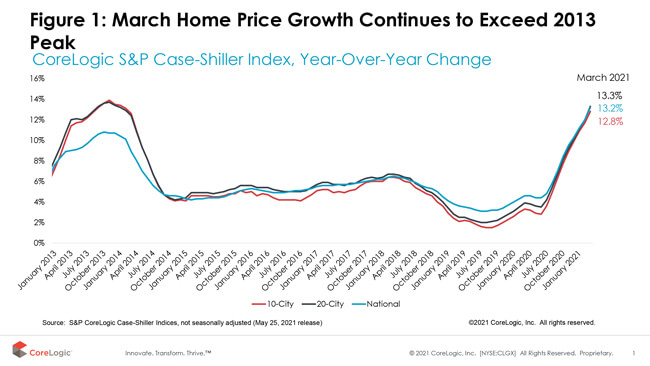

With consumer sentiment on the rise again and economic indicators suggesting accelerated demand ahead, S&P CoreLogic Case-Shiller Index pushed another double-digit increase — up 13.2% year over year in March. The month-to-month index jumped 1.95%, making it the strongest February-to-March increase in the recorded history of data.

While inventory challenges remain the focal point of housing market trends, and have been widely noted as a driver of price growth, it’s important to highlight the massive buildup in demand this year. Home price growth is trending 20% above 2017-to-2019 levels and is contributing to widespread bidding wars among buyers. The heightened demand is partially due to the wave of millennials reaching a critical juncture in their lives when their families are growing and they need more space. However, there is also a sense of rush among non-millennial buyers who may be feeling rapid price growth will put homes out of their reach soon. Some demand this spring might be spillover from last year’s prospective buyers who were left sitting on the sidelines when the pandemic brought the economy to a halt.

Unfortunately, the heightened demand is met by the dwindling availability of for-sale inventories, creating both the unique home buying environment we are facing this year and the continued acceleration in price growth. But, with demand in high gear and no respite in sight, home price growth is likely to remain in double digits over the coming quarter. This is also confirmed by the CME S&P Case Shiller Home Price Index futures, which is marking this month as its 15th anniversary of the first trades.

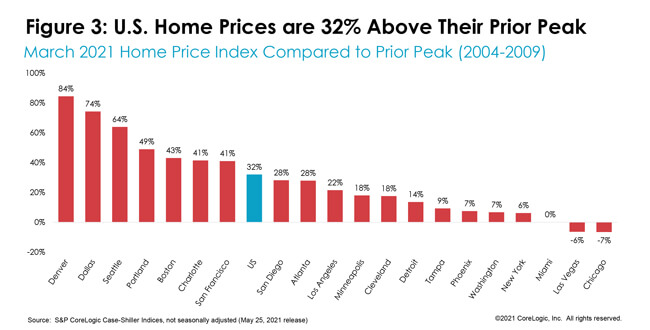

The 10- and 20-city composite indexes also continued the double-digit increase, up 12.3% and 13.3% year over year, respectively. The last time both indices had similar rates of growth was during the early months of 2014 (Figure 1). Compared to the prior peak, the 10-city composite is now 17% higher, while the 20-city composite is 22% higher than the previous peak both indexes reached in 2006.

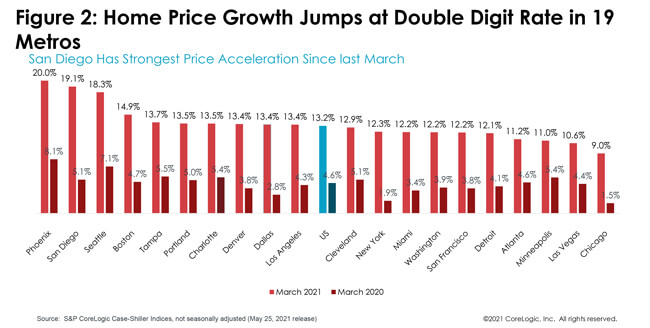

Ranking of metropolitan areas by price growth continued previous months’ trend. For the 21st consecutive month, Phoenix ranked with the fastest home price growth among the 20 markets — accelerating 20% in March — the fastest acceleration since May 2013 and 12-percentage points higher than the growth registered last March.

San Diego remained in second place for the fastest home price growth, with an annual increase of 19.1% and jumping 14-percentage points from last March’s increase. Seattle, in third place, had an 18.3% jump in March. Of the 20 cities, 19 experienced double-digit home price growth in March. However, Chicago and Las Vegas continued to lag, up 9% and 10.6%, respectively. These cities have been ranking lowest in price appreciation in recent months’ releases (Figure 2).

While the narrative has been focused on demand in non-coastal areas, coastal areas — such as San Francisco — are still flourishing with strong demand and experiencing double-digit home price jumps similar to the ones in more affordable metros.

In March, national home prices were 32% higher than the previous peak. Two cities that remain below their previous peaks are Las Vegas and Chicago, while Miami is now back to its previous peak. By contrast, Denver’s prices have jumped 84% above its 2006 peak, followed by Dallas at 74% (Figure 3).

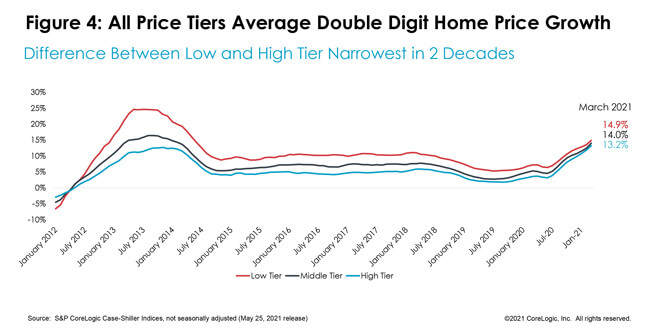

All three price tiers had double-digit growth for the third consecutive month. Prices of homes in the lower one-third of the price distribution jumped on average 14.9% in March. This is the strongest growth among the three tiers as demand for entry-level homes continues to be magnified by competition between first-time buyers, investors and baby boomers looking to downsize.

The average growth among medium-tier priced homes was not far behind at 14%, while prices in the highest-tier were up 13.2% on average. While higher-priced tiers are reaching the growth rates seen in 2013 — when the housing market was last showing similar rate of gains — the low tier is still at half of the growth rates seen in 2013 (at 25%). This was when that segment of the market was recovering from the foreclosure crisis and many were competing for significantly reduced prices.

As demand for homes in all price segments picked up pace since the onset of the pandemic, price growth between the low and high tier continued to draw closer, leading to the narrowest difference between the two in at least the last two decades (Figure 4).

The largest home price increases in the lower one-third tier continued to occur in Phoenix and Seattle, both up 20%, followed by an 18% increase in Atlanta and a 17% increase in New York, San Diego and Tampa, Florida. Compared to pre-pandemic rates in April 2020, price growth in New York’s low tier had the fastest acceleration of 13-percentage points, followed by San Francisco at 12-percentage points. In the high tier, San Diego’s price growth accelerated by 16.2-percentage points since last April, followed by a 13-percentage point acceleration in Seattle.

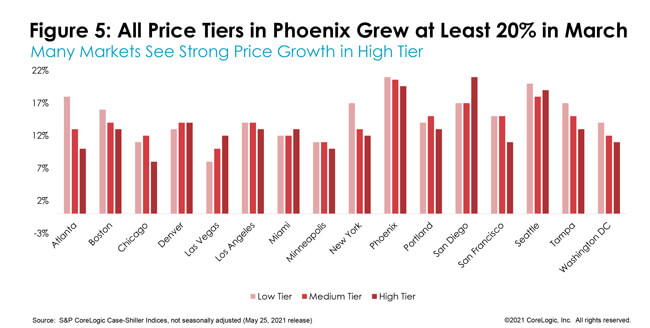

This March, San Diego had the fastest acceleration in the high tier among all recorded cities and compared to its lower price tiers, jumping 21% (Figure 5).

Massive home buying demand shows no signs of abating despite some rise in mortgage rates and concerns over overheated price growth. At the same time, hopes that new listings would proliferate as mass vaccinations encourage baby boomers to list their homes is also showing little signs of taking place. Thus, pressures on home prices continue to mount. And while continued price acceleration may raise concerns over sustainability, it is encouraging to see the strength and resiliency of U.S. consumers, especially following the deep economic decline they experienced last year. Part of the accelerated price growth amid heightened demand may be reflecting some migration patterns, namely households from more expensive coastal areas moving to more affordable ones, but also bringing with them higher price expectations that they are willing to pay.

Annual housing market comparisons over the next several months should be taken cautiously as the market was upended by the onset of the pandemic last year. Hence, comparisons to 2019 and 2018 will serve as a more reliable guide. Nevertheless, double-digit price growth is likely to slow down by the end of the year to single-digit growth.

©2021 CoreLogic, Inc. All rights reserved.