A Look Back at Another Episode of Reference Rate Replacement for an Adjustable-Rate HECM

A transition from London Interbank Offered Rate (LIBOR) to Secured Overnight Financing Rate (SOFR) as the new benchmark rate is well underway. Since the publication of SOFR in April 2018, average daily trading volume of SOFR-referenced floating rate securities nearly doubled from $618 billion to $1.1 trillion[1]. SOFR product offerings have since expanded to interest rate futures and interest rate swaps between SOFR and existing benchmarks such as LIBOR and Fed Funds[2]. A continued growth of SOFR futures and swaps market is crucial for a smooth transition.

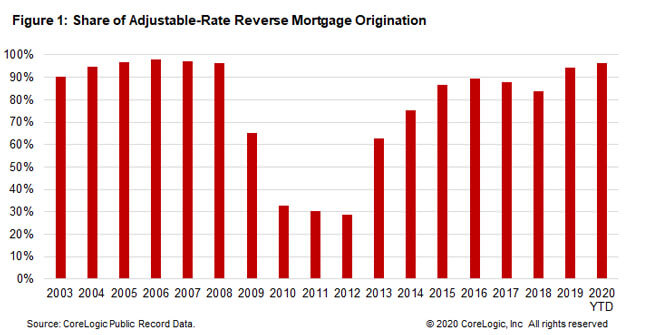

Nearly 95% of HECM loans are adjustable-rate loans (Figure 1). Today they are typically indexed to LIBOR, which wasn’t the case a little over a decade ago. The Treasury security yield was originally designated as the index rate for setting the interest rate for floating-rate HECM products. Accrued interest on the loan’s outstanding balance is calculated based on the 1-month or 12-month Treasury yield (that is, Constant Maturity Treasuries, CMT), plus a margin. While the margin – which may vary from lender to lender as well as from borrower to borrower- remains locked-in throughout the life of the loan, the base rate is indexed to, and moves with, CMT yields and is adjusted on a monthly or annual basis per the contract’s designation.

That changed in 2007 when the Department of Housing and Urban Development allowed the addition of LIBOR, as LIBOR is widely referenced in financial contracts (for example, bonds, derivatives, commercial paper), as well as in consumer lending such as adjustable-rate mortgages. Quoted in the interbank market, LIBOR is often regarded as a better indicator of the average rate at which banks and institutional borrowers could borrow from other banks or from the capital market. The new LIBOR option quickly replaced CMT yields to become the primary reference rate for an adjustable-rate HECM.

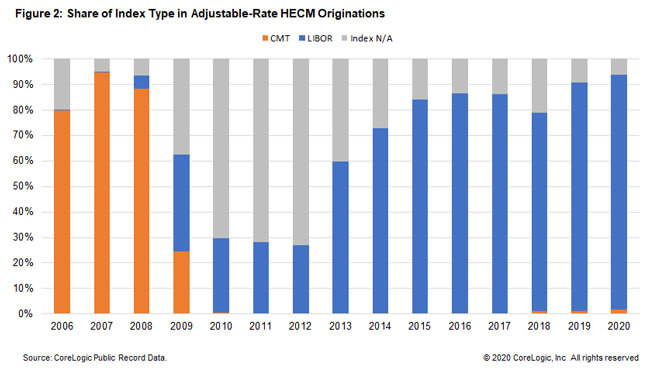

See Figure 2, where a review of CoreLogic Public Record data on reverse mortgages shows that the 2007 policy change led to a quick transition away from CMT. By 2009, there were more LIBOR-indexed adjustable-rate HECM loans than indexed to CMT yields, and by 2010, CMT-indexed loans had virtually disappeared from the tabulations. During 2010-2012 a large percentage of the HECM loans had missing index information, so it is difficult to determine the relative significance between LIBOR- and CMT-indexed originations. But a comparison with more recent years’ originations put the share of LIBOR-indexed adjustable-rate HECM loans at 80-90% since 2015.

One unique feature of an adjustable-rate HECM is that unlike a forward adjustable-rate mortgage, it relies on a short-term as well as a long-term reference rate. The short-term reference rate, such as the 1-month or 12-month CMT or LIBOR, is the basis for forward calculation of accrued interest on the loan balance which grows over time, whereas the long-term rate such as a 10-year CMT yield or 10-year LIBOR swap rate is the basis for backward calculation to determine the amount available to borrowers at the time a loan is made.

The 2007 transition from CMT to LIBOR was largely smooth and swift as there were well-developed LIBOR spot and derivatives products as well as a LIBOR term structure. While a continued growth in volume and depth of a SOFR futures and swaps market will increase the adoption of SOFR, more is to be known as to how SOFR instruments may perform, say, relative to similar maturity LIBOR instruments.

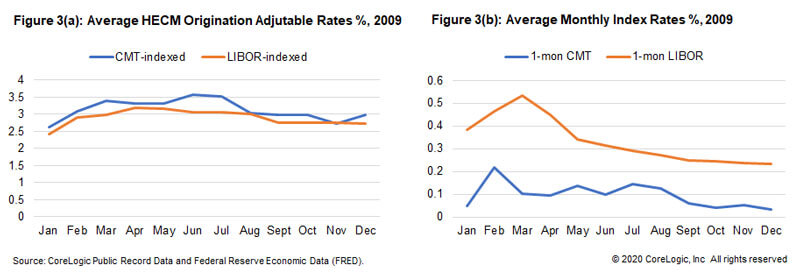

In the two years from April 2018 to March 2020, the SOFR has averaged 0.10% or 10 basis points below the 1-month LIBOR and 46 basis points below the 12-month LIBOR, partly reflecting SOFR’s collateralized borrowing. But a lower average base rate doesn’t always mean it will pass through onto borrowers unless it closely reflects the lender’s cost of funding the loans. Any shortfall relative to the funding cost will be reflected in a higher margin above the index. A case in point: Figure 3, which shows a time period (2009) when both the CMT and LIBOR were commonly used in HECM adjustable-rate contracts. Average interest rates on CMT-index contracts were generally higher than those indexed to LIBOR despite lower CMT yields than LIBOR rates, reflecting a higher margin used in CMT-indexed contracts.

With less than two years before LIBOR is scheduled to sunset, we can expect continued growth in the issuance of SOFR products to drive greater market acceptance of SOFR. Today the reverse mortgage market is largely dominated by companies that specialize in reverse mortgage lending. Will these lenders find the cost and availability of funds in the repo market adequately reflect their access to credit, which is often in the form of a warehouse line of credit? What about small banks and independent mortgage companies who may or may not offer the loans as a correspondent to large wholesale lenders? A better understanding of lenders’ funding conditions will help regulators and the lending community at large better prepare for the transition away from LIBOR.

©2020 CoreLogic,Inc. All rights reserved.

[1] Source: the New York Federal Reserve Bank website.

[2] Source: the CME Group website.