Home / Intelligence / Loan Performance Insights – September 2023

Loan Performance Insights – September 2023

September 28, 2023

Introduction

The CoreLogic Loan Performance Insights report features an interactive view of our mortgage performance analysis through July 2023.

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To more comprehensively monitor mortgage performance, CoreLogic examines all stages of delinquency as well as transition rates that indicate the percent of mortgages moving from one stage of delinquency to the next.

The report is published monthly with coverage at the national, state and Core Based Statistical Area (CBSA)/Metro level and includes transition rates between states of delinquency and separate breakouts for 120+ day delinquency.

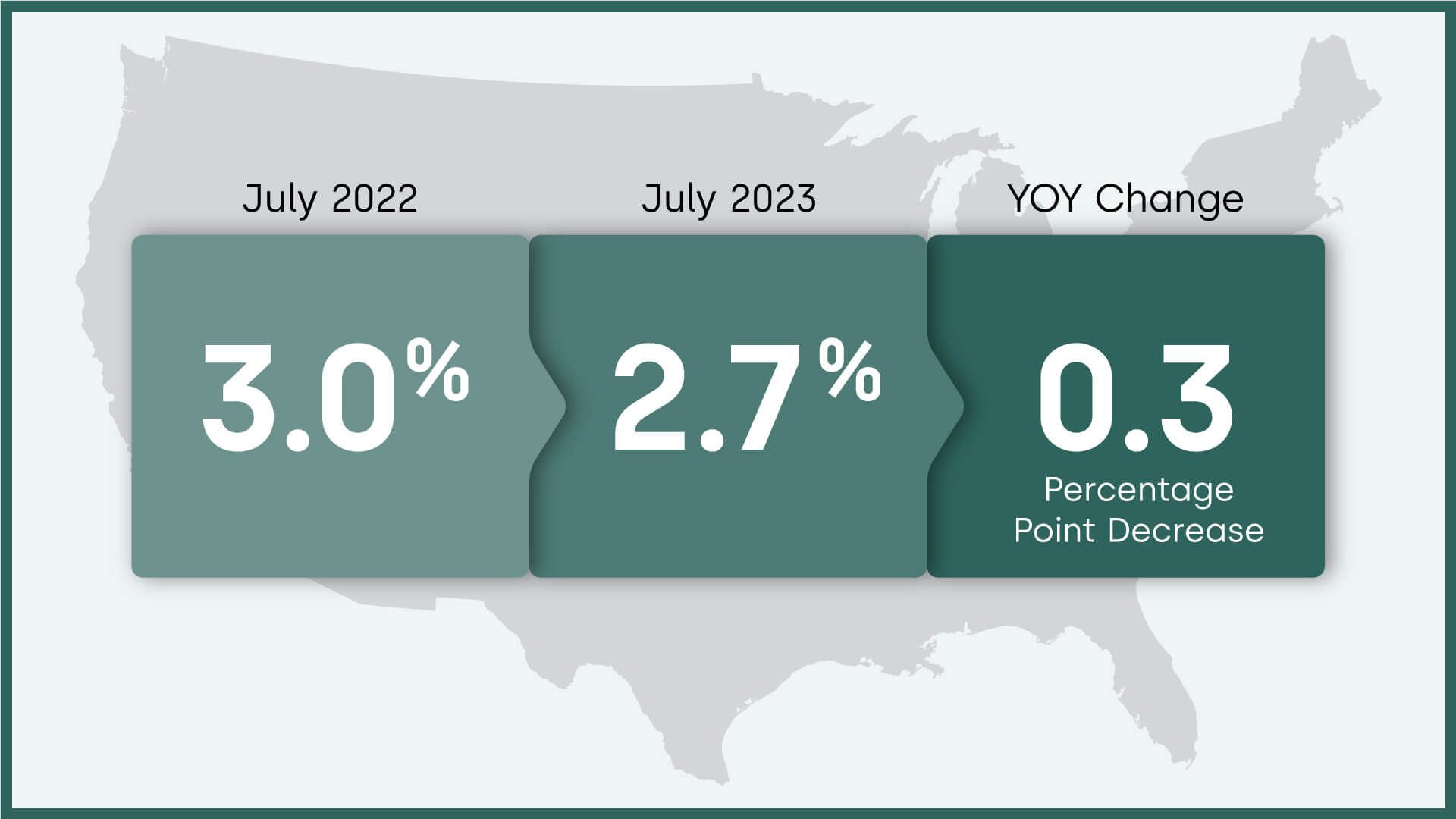

Chart 1: Overall U.S. mortgage delinquency rate and year-over-year change, July 2023

“Overall U.S. mortgage delinquencies remained near a record low in July, with the share of homes entering that status or progressing to later stages either unchanged or lower. Since most borrowers have substantial amounts of home equity, those who have locked in low mortgage rates that do enter later stages of delinquency will most likely not experience foreclosures.And while home equity gains have slowed from their former rapid pace, CoreLogic projects that home price growth will pick up over the next year. Borrowers should continue to build equity over the coming months, even if at a more moderate rate.”

-Molly Boesel

Principal Economist for CoreLogic

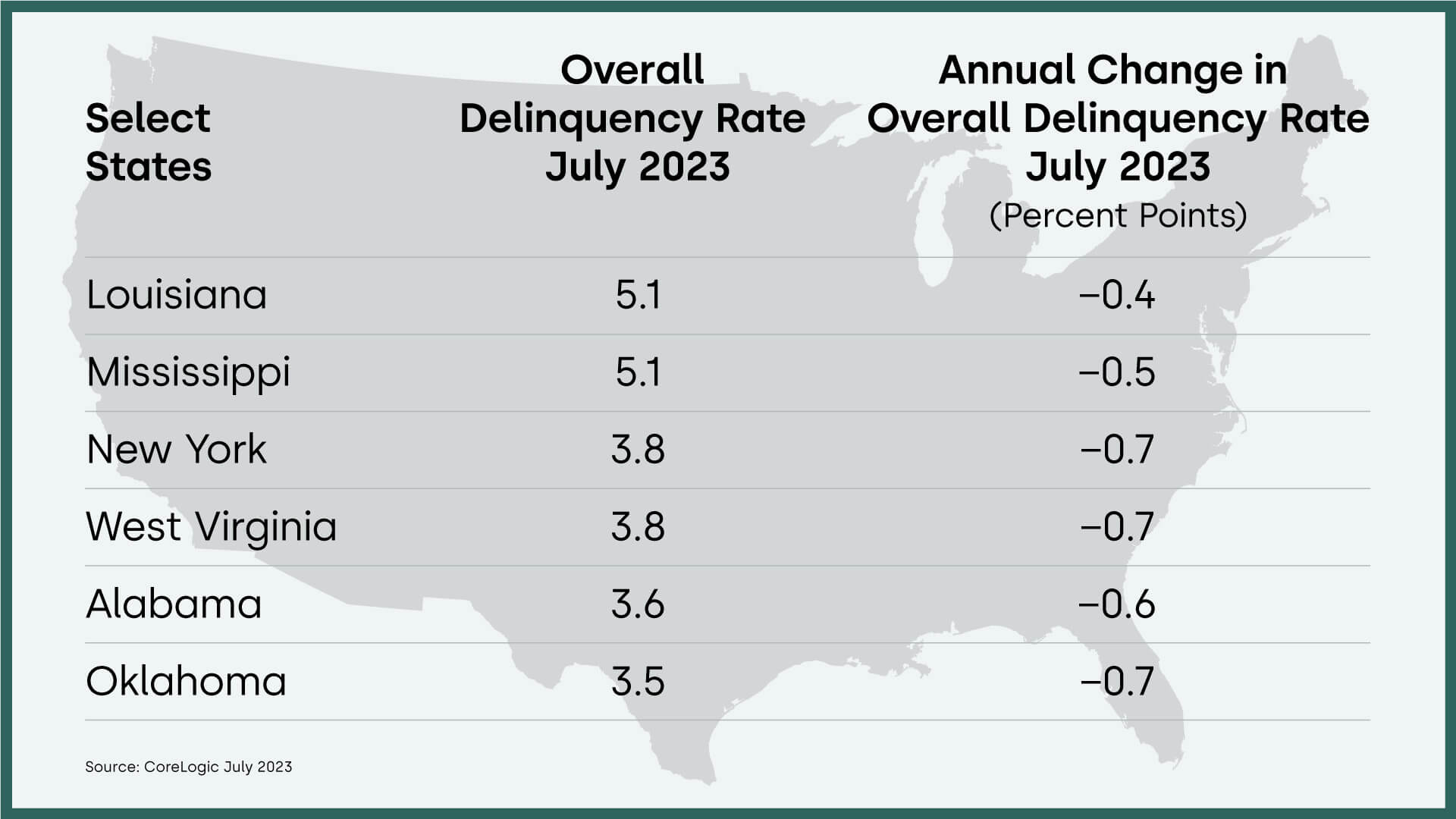

Chart 2: Overall U.S. mortgage delinquency rate by select state and year-over-year change, July 2023

30 Days or More Delinquent – National

In July 2023, 2.7% of mortgages were delinquent by at least 30 days or more including those in foreclosure. This represents a 0.3 percentage point decrease in the overall delinquency rate compared with July 2022.

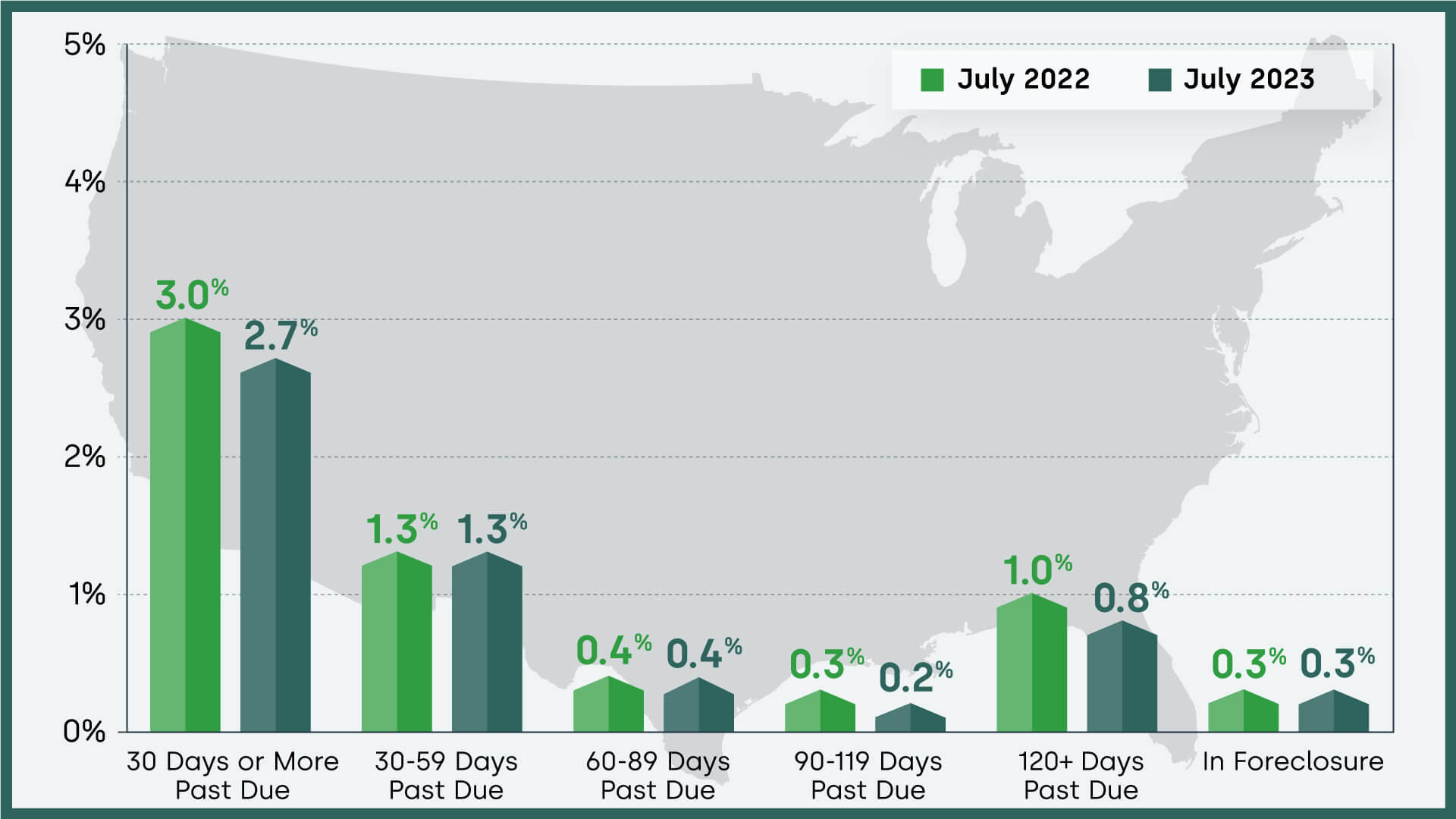

Chart 3: U.S. mortgage delinquency rates by time frame and year-over-year change, July 2023

Only One State Posts a Small Overall Annual Delinquency Rate Increase in July

U.S. mortgage performance held strong in July, with both overall delinquency and foreclosure rates still hovering near record lows. Only Idaho saw overall delinquencies rise year over year, but rates in that state remain very low. Meanwhile 16 metro areas posted slight annual delinquency upticks, a drop from the previous month, when 31 metros posted increases. With hurricane season in full swing in the late summer and early fall, some areas of the U.S. could see typical seasonal delinquencies rise later this year and into 2024.

Loan Performance – National

CoreLogic examines all stages of delinquency to more comprehensively monitor mortgage performance.

The nation’s overall delinquency rate for July was 2.7%. The rate for early-stage delinquencies – defined as 30 to 59 days past due – was 1.3% in July 2023, unchanged from July 2022. The share of mortgages 60 to 89 days past due was 0.4%, unchanged from July 2022. The serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – was 1% down from 1.3% in July 2022.

As of July 2023, the foreclosure inventory rate was 0.3%, unchanged from July 2022.

Transition Rates – National

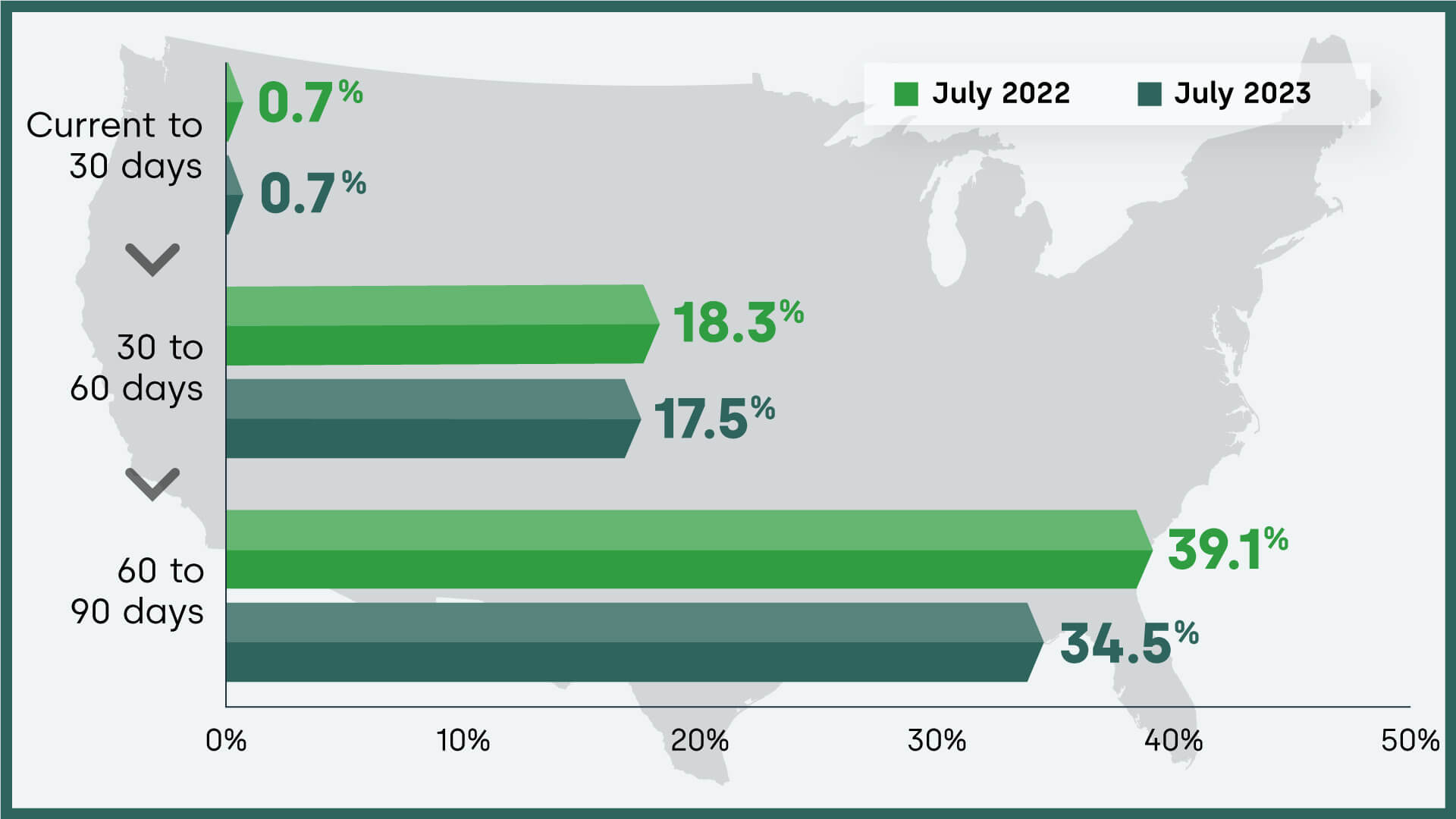

CoreLogic examines all stages of delinquency as well as transition rates that indicate the percent of mortgages moving from one stage of delinquency to the next.

The share of mortgages that transitioned from current to 30-days past due was 0.7%, unchanged from July 2022.

Chart 4: Share of delinquent mortgages transitioning from one stage to the next and year-over-year change, July 2023

Overall Delinquency – State

In July 2023, one state (Idaho) posted a small year-over-year increases in its overall delinquency rate, while two states (Arizona and Utah) were unchanged. The states and districts with the largest declines were Alaska, New York, Oklahoma and West Virginia.

Chart 5: Year-over-year change in overall mortgage delinquency rate by all states and districts, July 2023

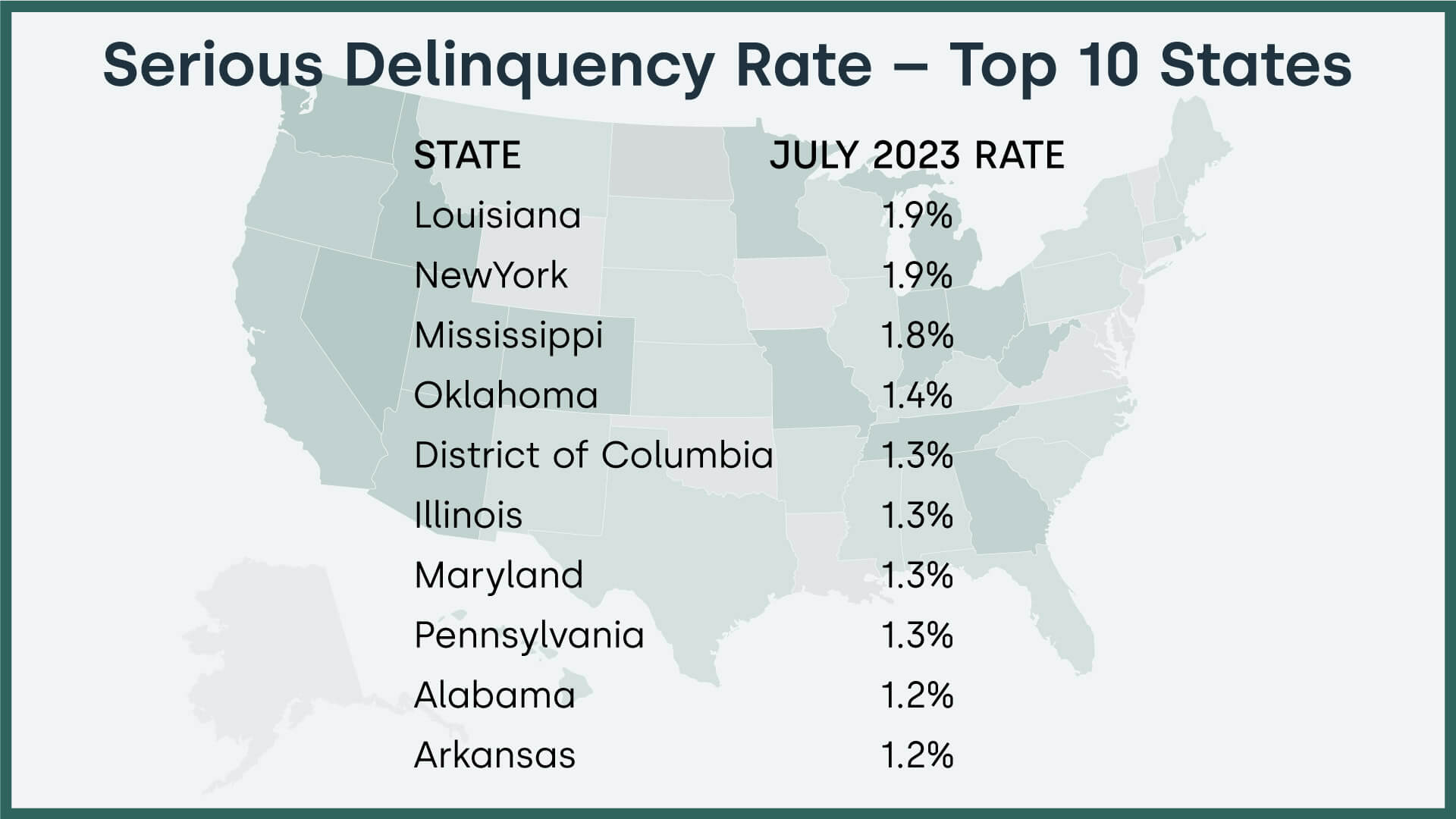

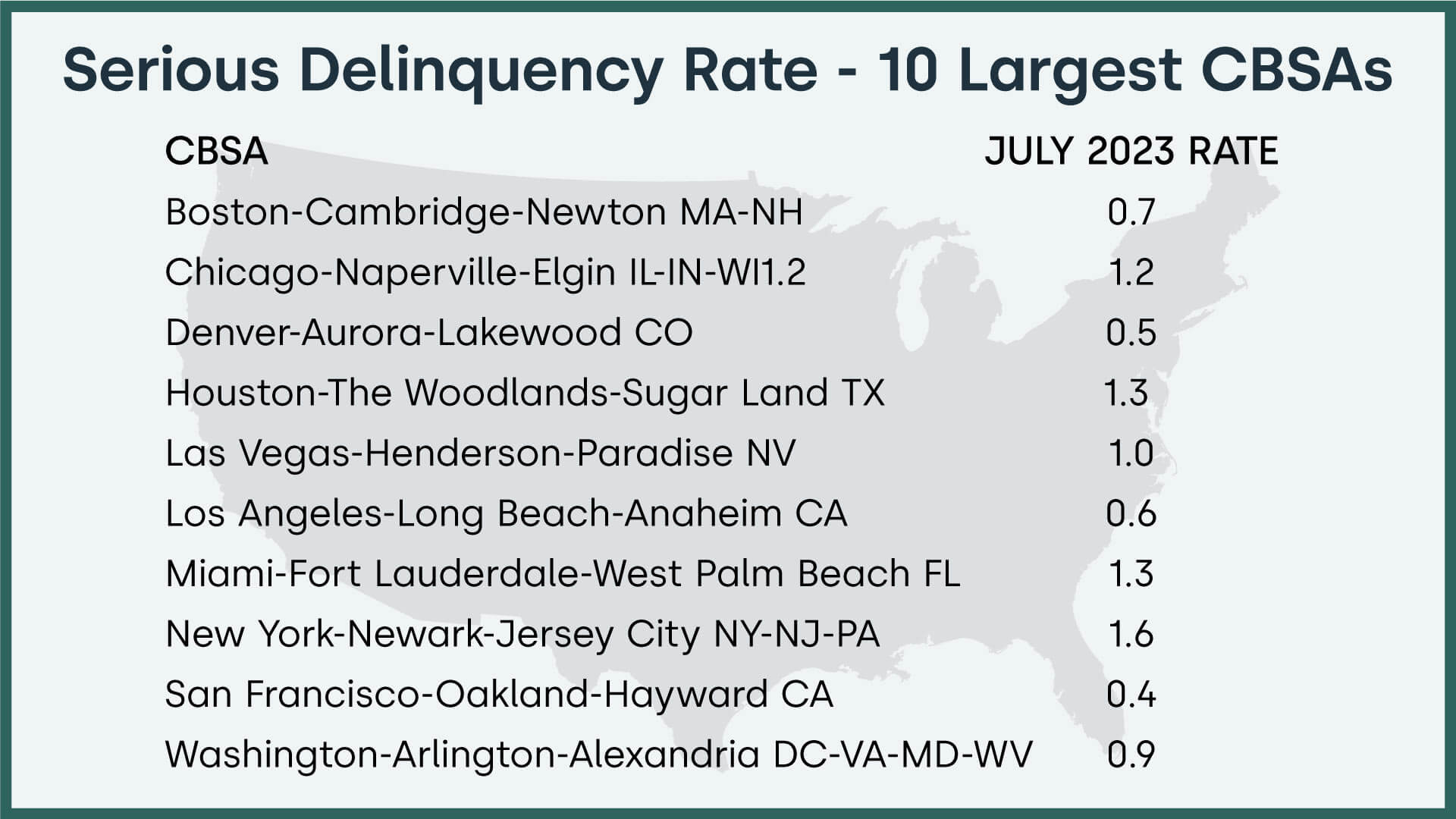

Serious Delinquency – Metropolitan Areas

Serious delinquency is defined as 90 days or more past due including loans in foreclosure.

There were two metropolitan areas where the serious delinquency rate increased.

There were 12 metropolitan areas where the serious delinquency rate stayed the same.

There were 370 metropolitan areas where the serious delinquency rate decreased.

Chart 6: Year-over-year change in serious mortgage delinquency rate by metro area, July 2023

Summary

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To more comprehensively monitor mortgage performance, CoreLogic examines all stages of delinquency as well as transition rates that indicate the percent of mortgages moving from one stage of delinquency to the next.

The data in this report represents foreclosure and delinquency activity reported through July 2023. The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure and are, therefore, excluded from the analysis. Approximately one-third of homes nationally are owned outright and do not have a mortgage. CoreLogic has approximately 75% coverage of U.S. foreclosure data.

Source: CoreLogic

The data provided are for use only by the primary recipient or the primary recipient’s publication or broadcast. This data may not be resold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data are illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Robin Wachner at [email protected]. For sales inquiries, please visit https://www.corelogic.com/support/sales-contact/. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. The data are compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic, the leading provider of property insights and solutions, promotes a healthy housing market and thriving communities. Through its enhanced property data solutions, services and technologies, CoreLogic enables real estate professionals, financial institutions, insurance carriers, government agencies and other housing market participants to help millions of people find, buy and protect their homes. For more information, please visit www.corelogic.com.

CORELOGIC, the CoreLogic logo, CoreLogic LPI and CoreLogic LPI Forecast are trademarks of CoreLogic, Inc. and/or its subsidiaries. All other trademarks are the property of their respective owners.

During the pandemic, some U.S. homebuyers relocated to areas that were more affordable or had better access to outdoor amenities, but this sometimes led to migration to riskier climates.