Hurricane Fiona, the first major hurricane of the 2022 season, made landfall in Nova Scotia and New Foundland on Saturday. Severe winds and rain are impacting Canada’s Atlantic Coast, leaving hundreds of thousands without electricity and destroying homes and businesses.

In this pre-landfall post, CoreLogic covered Hurricane Fiona’s forecasted path, the probability of hurricane-force winds in Atlantic Canada, floor risk score maps for impacted cities, and the number of buildings that could be at risk to flood. Now that the hurricane has arrived, we can take a look at some of the properties that have been impacted and their associated flood risk score. Channel-Port aux Basques, a town in Newfoundland and Labrador, Canada, was particularly impacted.

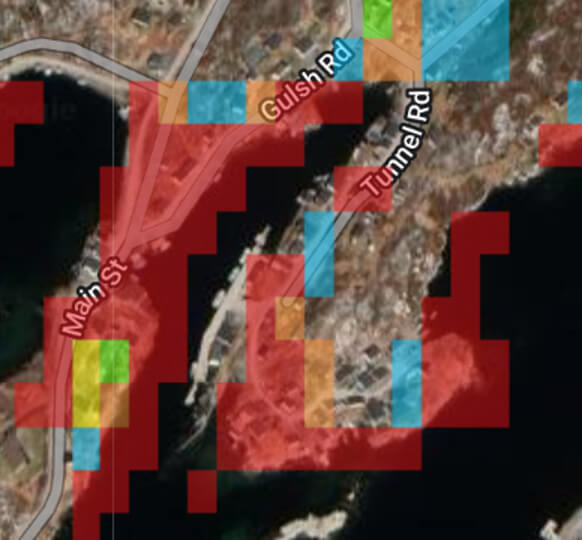

The red property below in Rose Blanche-Harbour le Cou, a town 45kim east of Port aux Basques, is an example:

https://ottawa.citynews.ca/local-news/after-fiona-storm-recovery-begins-as-police-confirm-first-fatality-5870138 (Pauline Billard via AP)

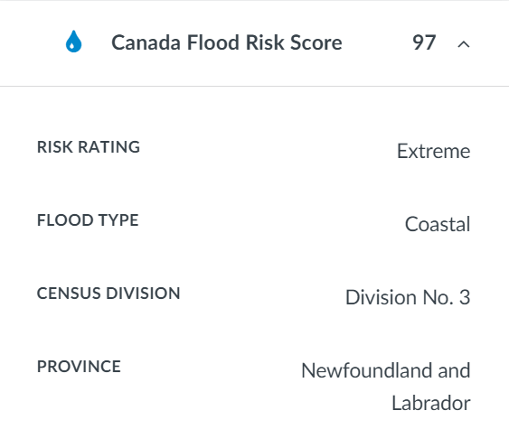

This property was rated by CoreLogic RiskMeter with an extreme flood risk of 97 (1-100 scale).

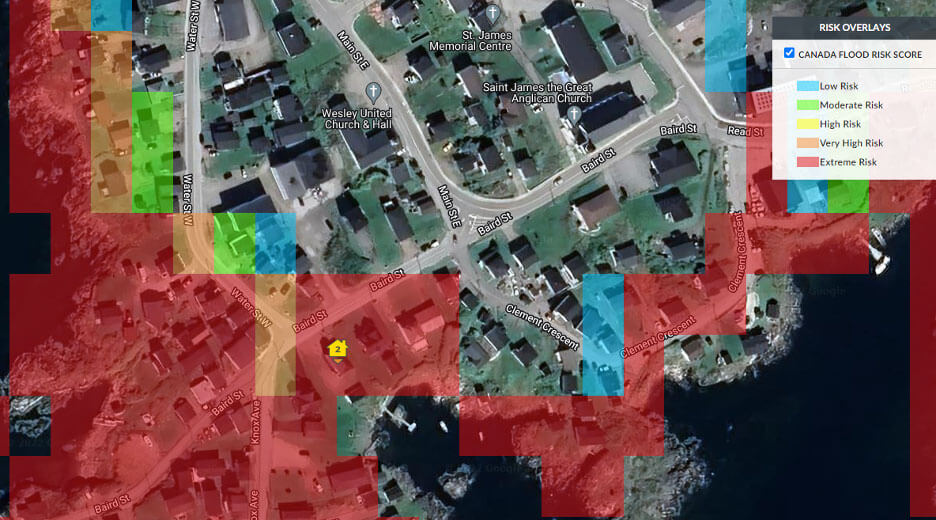

Another property, pictured below near the Anglican Church in Port aux Basques, experienced damage:

https://www.cbc.ca/news/canada/newfoundland-labrador/port-aux-basques-fiona-september-27-1.6597027 (Yan Theoret, CBC)

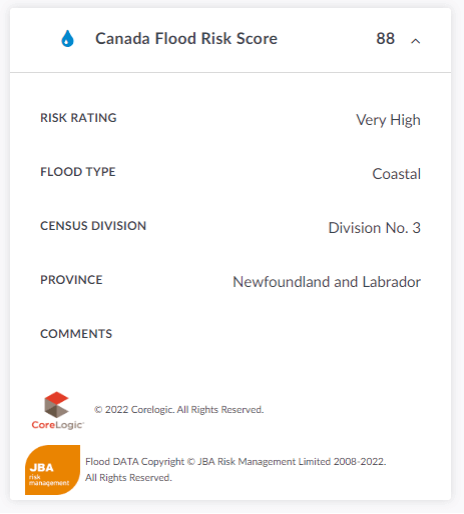

This property was rated by CoreLogic RiskMeter with a very high flood risk of 88 (1-100 scale).

The CoreLogic Flood Risk Score for Canada includes coastal, flash and riverine flooding. The scores leverage detailed hydrological and hydraulic modeling analyses, which were validated against river gauge data, local engineering studies and flood maps. The flood risk scores account for local flood defenses such as levees and sea walls.

Flooding poses significant risk to vulnerable properties. Fiona caused considerable damages and power loss, and ongoing supply chain issues and inflation are going to make the recovery more challenging. These events will continue to happen, and it’s more important than ever for homeowners and insurers to use this data to be able to assess how vulnerable any given property is to these disasters.