- Preceding the global coronavirus (COVID-19) outbreak, overall delinquency rates in January reached their lowest level in more than 20 years

- The U.S. serious delinquency rate in January remained at its lowest level since April 2000

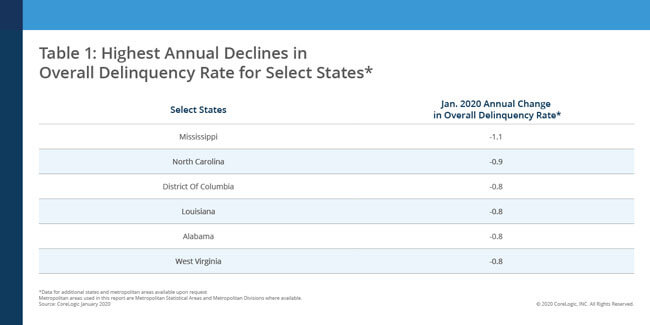

- North Carolina and Mississippi posted the largest annual declines in overall delinquency rates

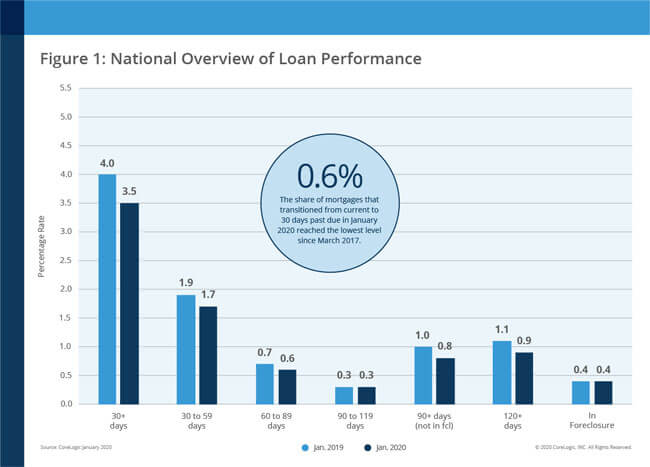

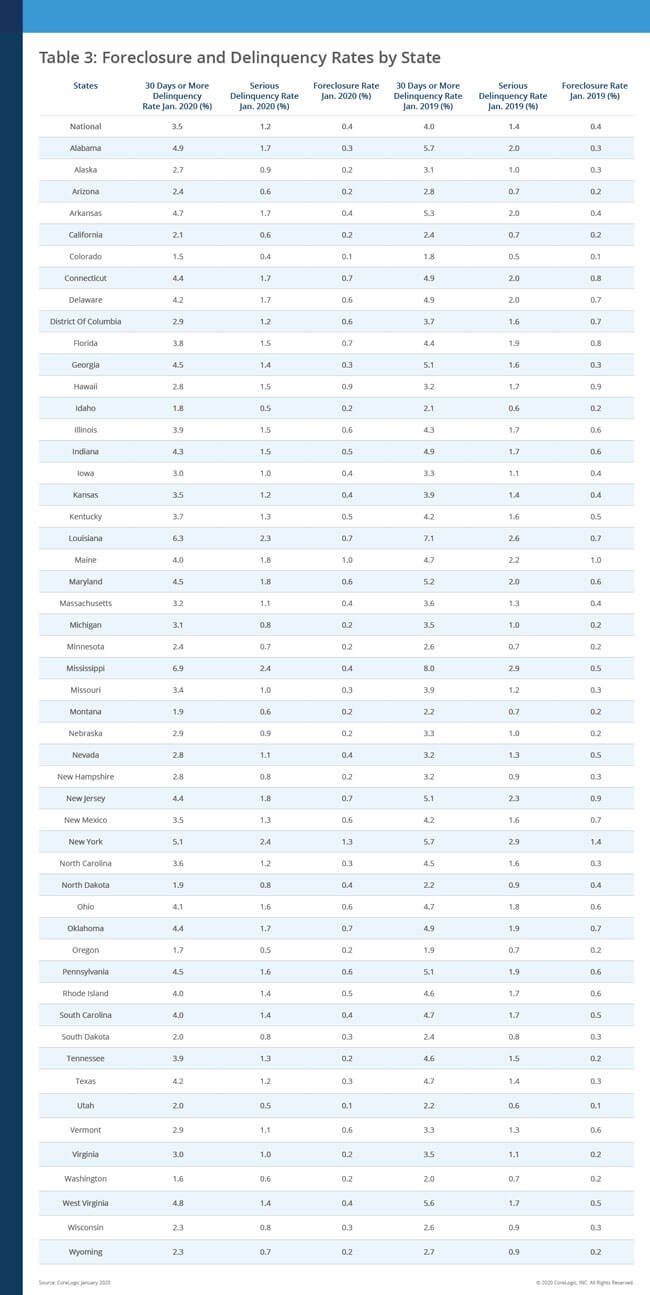

CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report. The report shows that nationally, 3.5% of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure) in January 2020, representing a 0.5 percentage point decline in the overall delinquency rate compared with January 2019, when it was 4%. This marked 25 consecutive months of annual declines and was the lowest for a January in more than 20 years.

The mortgage market experienced a strong year of improvement in loan performance during 2019 – carrying over into the first month of 2020. However, mounting job losses since the COVID-19 pandemic was declared a national emergency has raised the possibility of many borrowers falling behind on their mortgage payments in coming months.

“Home loan delinquency and foreclosure rates were the lowest in a generation before the COVID-19 pandemic hit,” said Dr. Frank Nothaft, chief economist at CoreLogic. “Recession-induced job losses will fuel delinquencies. However, wide-spread foreclosures across America will likely be averted because of the home equity buffer that homeowners have and the available forbearance programs. Our Home Equity Report found that at the start of 2020, homeowners with a mortgage also had an average of $177,000 in home equity.”

As of January 2020, the foreclosure inventory rate, which measures the share of mortgages in some stage of the foreclosure process, was 0.4% – unchanged from January 2019. January’s foreclosure inventory rate tied the prior 14 months as the lowest for any month since at least January 1999.

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To monitor mortgage performance comprehensively, CoreLogic examines all stages of delinquency, as well as transition rates, which indicate the percentage of mortgages moving from one stage of delinquency to the next.

The rate for early-stage delinquencies – defined as 30 to 59 days past due – was 1.7% in January, down from 1.9% in January 2019. The share of mortgages 60 to 89 days past due in January was 0.6%, down from 0.7% in January 2019. The serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – was 1.2% in January, down from 1.4% in January 2019. This is the lowest serious delinquency rate experienced since April 2000, when it was 1%.

Since early-stage delinquencies can be volatile, CoreLogic also analyzes transition rates. The share of mortgages that transitioned from current to 30 days past due was 0.6% in January 2020, down from 0.8% in January 2019. By comparison, just before the start of the financial crisis in January 2007, the current-to-30-day transition rate was 1.2%, and peaked at 2% in November 2008.

“After some initial cushioning from equity buffers, lower mortgage interest costs and government support and forbearance programs, we expect delinquency rates to jump significantly throughout the year as the economic toll from COVID-19 becomes more evident,” said Frank Martell, President and CEO of CoreLogic. “It is likely that areas of the country that have local economies driven by energy, transportation and media and entertainment will lead the way in delinquencies. The ultimate extent of the higher delinquencies will depend on how quickly the broader economy opens up again and employment levels rebound – both of these factors are uncertain at this time.”

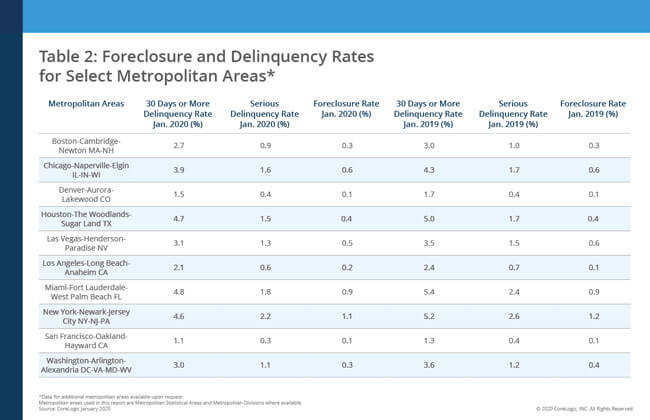

In January, for the fifth consecutive month, no states posted a year-over-year increase in the overall delinquency rate and Mississippi (down 1.1 percentage points) and North Carolina (down 0.9 percentage points) recorded the largest declines. In addition, only three metropolitan areas recorded small increases in overall delinquency rates.

The next CoreLogic Loan Performance Insights Report will be released on May 12, 2020, featuring data for February 2020.

For ongoing housing trends and data, visit the CoreLogic Insights Blog: www.corelogic.com/insights.

Methodology

The data in this report represents foreclosure and delinquency activity reported through January 2020.

The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not typically subject to foreclosure and are, therefore, excluded from the analysis. Approximately one-third of homes nationally are owned outright and do not have a mortgage. CoreLogic has approximately 85% coverage of U.S. foreclosure data.

Source: CoreLogic

The data provided is for use only by the primary recipient or the primary recipient’s publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Allyse Sanchez at [email protected]. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic (NYSE: CLGX), the leading provider of property insights and solutions, promotes a healthy housing market and thriving communities. Through its enhanced property data solutions, services and technologies, CoreLogic enables real estate professionals, financial institutions, insurance carriers, government agencies and other housing market participants to help millions of people find, acquire and protect their homes. For more information, please visit www.corelogic.com.

CORELOGIC and the CoreLogic logo are trademarks of CoreLogic, Inc. and/or its subsidiaries. All other trademarks are the property of their respective owners.

Media Contact

Allyse Sanchez

INK Communications

925-548-2535

[email protected]