Economic Observations, March 2019

Lately, it seems like the roof of the housing market might cave in. Several of the major housing market indicators have shown much volatility as of late. For instance, the S&P CoreLogic Case-Shiller Home Price Index fell for seven straight months, new home sales dropped a whopping 12 percent at the end of last year, and inventory is starting rise. On top of that, we’re six month’s short of the longest economic expansion. As such, it is understandable why some might think that the housing market and broader cycle is coming to an end.

Despite these troublesome signs, there are several reasons to be optimistic that the housing market is in good shape to weather a downturn.

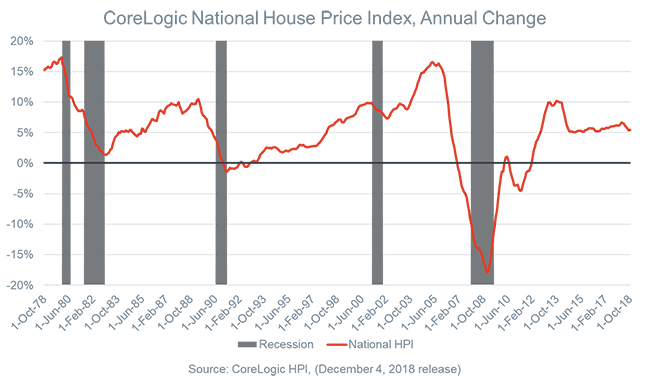

First, broad and deep troughs in housing prices is the exception, rather than the rule, during recessions. If we look at the past five recessions, we see that home prices typically weather down turns quite well. For example, home prices grew 6.6 percent during the Dot-Com recession in 2001. And during the 1980 and 1981 recessions, prices grew by 6.1 percent and 3.5 percent, respectively. In fact, just two of the past five recessions brought decreases in home prices: a small 1.9 percent drop during the 1991 recession, and, of course, the massive 19.7 percent price drop during the Great Recession.

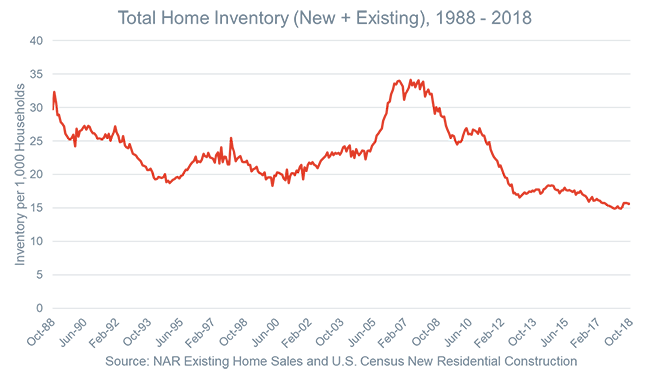

Second, housing inventory struggles to keep pace with demand. Total single-family inventory, which is the sum of newly-built and used homes, sits at just 15.7 homes per 1,000 household. This is up slightly from the record low of 14.9 set in December 2017. The fact that we’re at historically low inventory is important because it means we’re in a very different supply environment compared to the massive run up in inventory that appeared before the onset of the Great Recession. Today’s low supply environment means that prices are unlikely to fall far, if at all, during the next recession.

Lastly, the demographic structure of the United States should continue to support prime-household growth for over the next two decades. Currently, just under 46 percent of the U.S. population is under 35. As this cohort ages and gets their housing-market sea legs, we should expect them to form new households as they enter into their peak marital and child-bearing years. For example, The Harvard Joint Center for Housing Studies estimates Millennial households are expected to grow by 32 million over the next twenty years. That’s a lot of new homes that will be needed, regardless of whether they buy or rent. This surge in demand should continue to put upward pressure on the housing market until at least 2040.

© 2019 CoreLogic, Inc. All rights reserved.