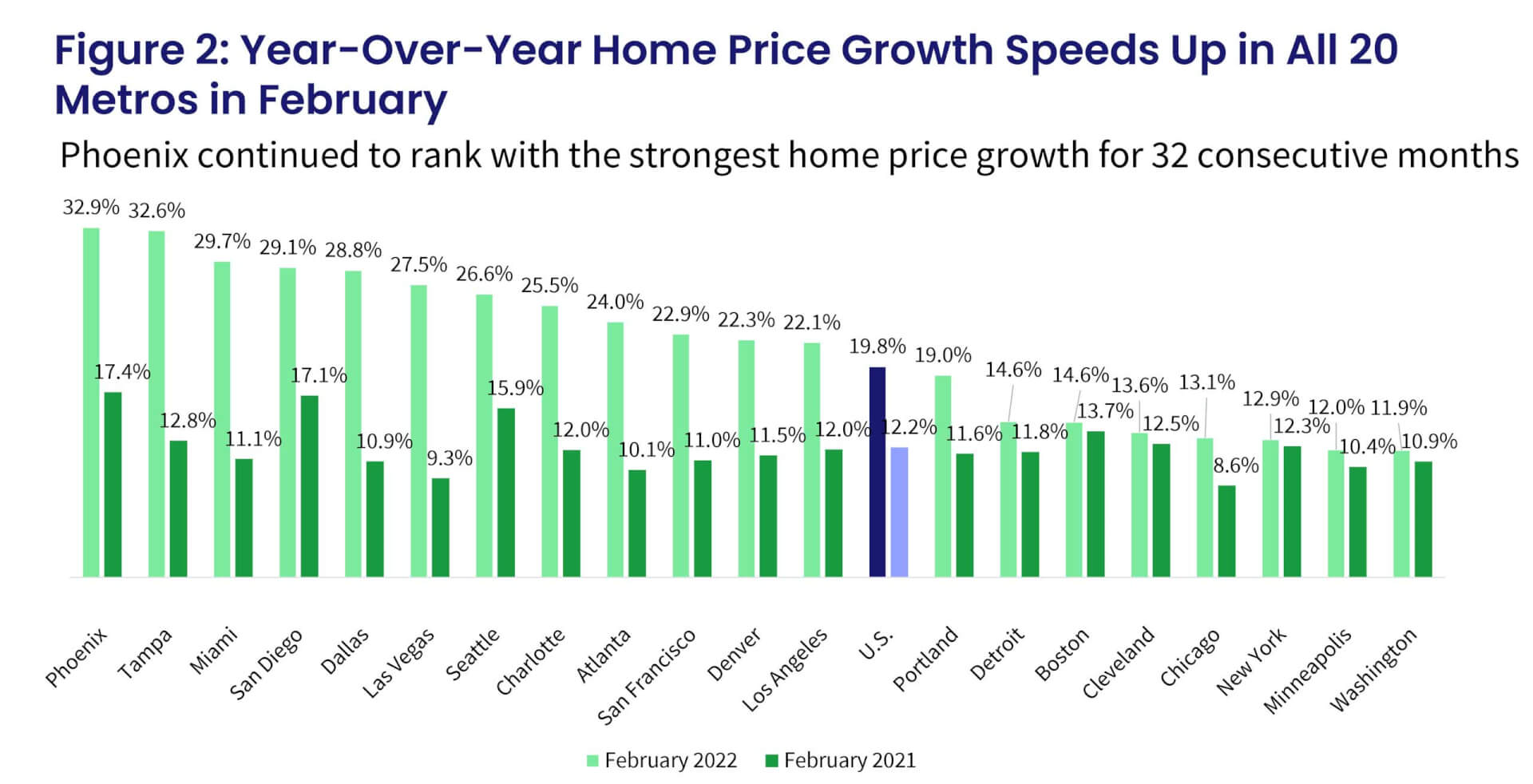

In February, all 20 metro areas showed stronger annual home price growth compared to January

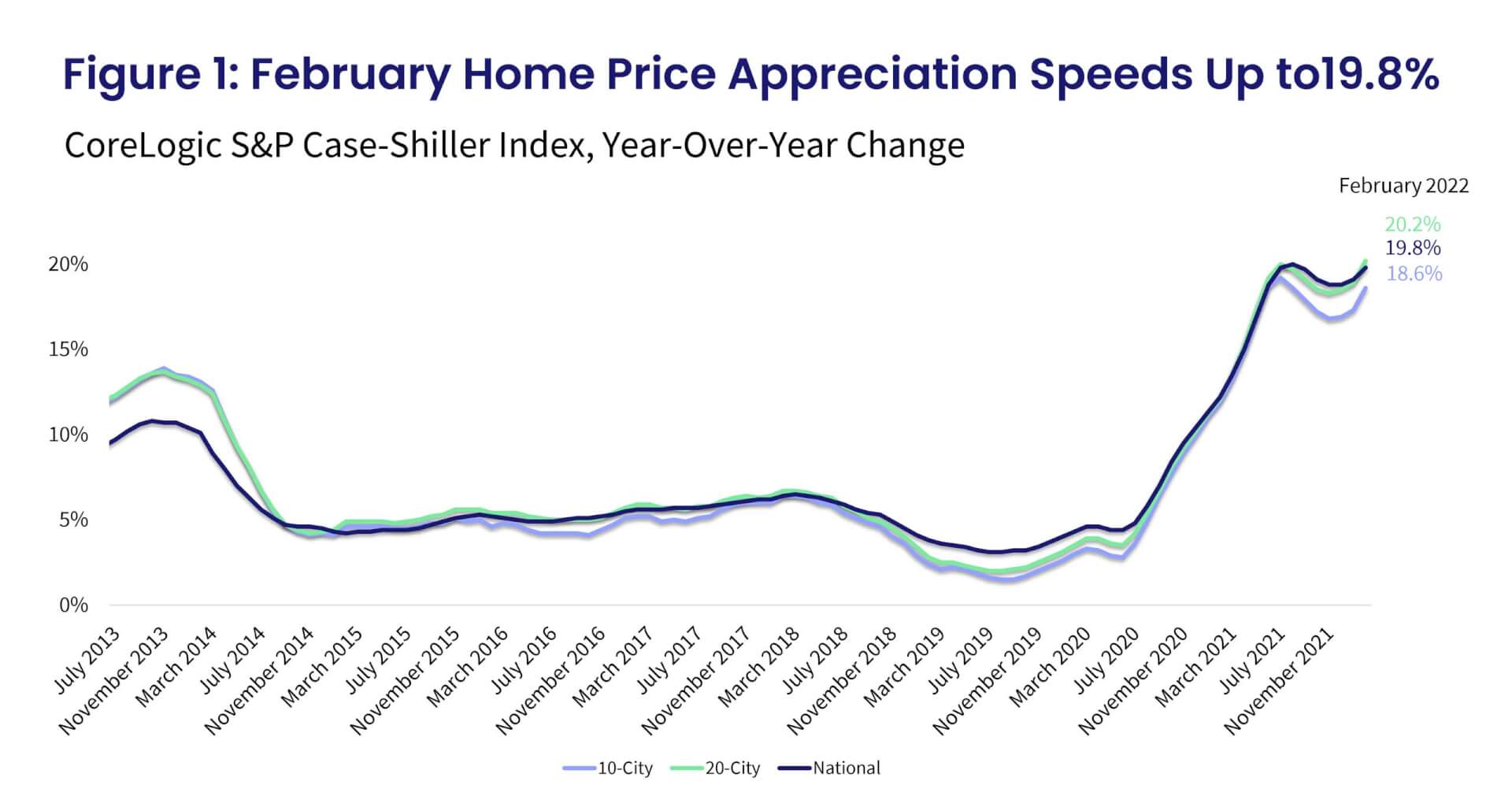

Home price growth continued to gain speed in early spring, as eager buyers tried to get in front of the mortgage rate surge. The S&P CoreLogic Case-Shiller Index posted a 19.8% increase in February, the second month of accelerated growth after a winter lull. This was the strongest February year-over-year increase since the beginning of the data series.

Concerns about higher mortgage rates propelled much of the spring homebuying demand, which was not, however, met with a comparable increase in new inventory. Continued pressure on home prices drove growth to new historic highs. Nevertheless, with mortgage rates rising above 5% in recent weeks and diminishing buying power, home price growth is likely to recede in coming months.

The non-seasonally adjusted month-to-month index also surged, up 1.73% — also the largest monthly increase in the data series. Between 2015 and 2020, the monthly index changes from January to February averaged about 0.24%.

The 10- and 20-city composite indexes also marched upward to new highs, surging 18.6% and 20.2% year over year, respectively (Figure 1). The gains remained higher in the 20-city index, as buyers with larger budgets continue to flock to smaller and more affordable areas, particularly those in Florida.

Compared to the 2006 peak, the 10-city composite is now 36% higher, while the 20-city composite is up 43%. Adjusted for inflation, which continues to remain elevated, the 10-city index is down 1%, while the 20-city index is up 5% compared to the 2006 peak.

For the 32nd consecutive month, Phoenix had the strongest annual home price growth among the 20 tracked markets, surging 32.9% in February, up from January’s non-seasonally adjusted rate of 32.6%.

Tampa, Florida, still ranks second, with a 32.6% year-over-year gain, up from 29.4% the month before. Miami ranks third, with a 29.7% increase in February. While Tampa and Miami have been competing for the second-highest growing cities over the last year, February’s re-acceleration was strongest in West Coast markets such as Los Angeles, San Francisco, Seattle and San Diego, all of which posted about a 2 percentage-point increase in annual gains since January. Phoenix, on the other hand, had one of the slowest monthly gains in year-over-year growth — only 0.27-percentage points from January. Minneapolis, New York and Cleveland also posted some of the slowest increases in annual gains.

Nevertheless, all 20 metro areas experienced acceleration in annual gains from January.

Washington and Minneapolis remained at the bottom of the year-over-year price growth list, up 11.9% and 12%, respectively. Despite having the slowest rate of annual price increases, these areas have still experienced double-digit growth rates for 15 consecutive months. (Figure 2).

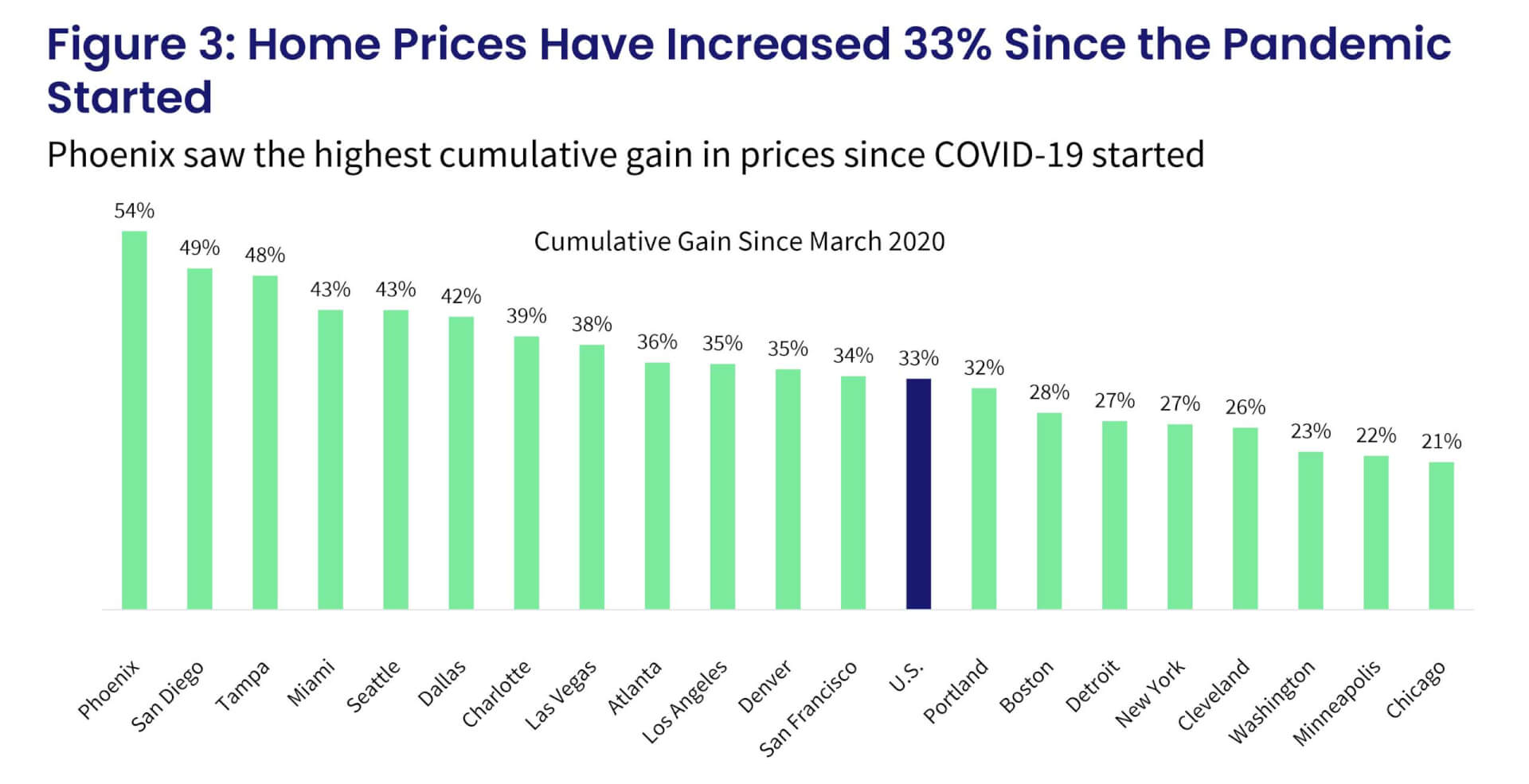

Cumulatively, home prices are up 33% since March 2020 when the pandemic started. Given the strength in the Phoenix market for the past 32 months, which started prior to the COVID-19 outbreak, prices are now up 54% compared to March 2020, the highest among the 20 metro areas tracked. San Diego follows with a 49% cumulative gain. In contrast, but in line with year-over-year trends observed in previous releases, Chicago, Minneapolis and Washington have had cumulative increases amounting to about 21% to 23% (Figure 3).

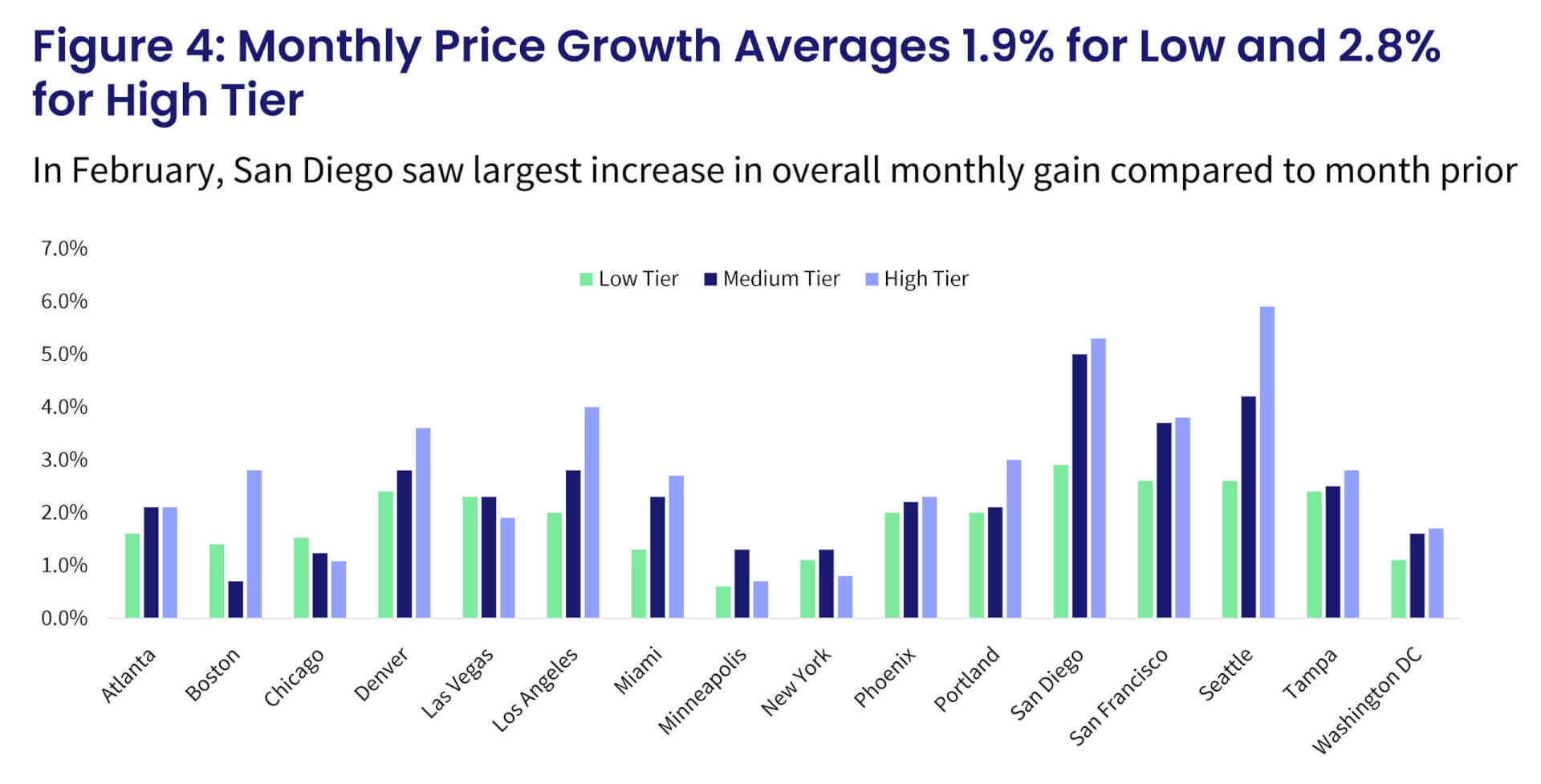

Furthermore, all three price tiers also continued to see stronger annual gains in February, with the high tier showing most of the acceleration, up 23% in February from 21.3% in January. The average growth in gains for low-tier homes lagged but was still up by 20.6%. The slowing price growth in the low tier reflects affordability challenges that home shoppers in this price range face after almost two years of vigorous price gains and an increase in mortgage rates — in addition to low inventory.

Furthermore, the month-to-month comparison of home price growth by price tier and location reveals relative changes in demand across the country. From January to February, areas with colder climates, particularly Minneapolis, New York and Chicago, continued to show smaller monthly increases. For the third consecutive month, all metros had at least some gains across the price tiers — although some of the growth can be attributed to seasonal patterns, since monthly increases are generally positive between January and February.

The largest monthly gains were in warmer areas and on the West Coast, including San Diego, Seattle and San Francisco, which were all up notably in February. San Diego and San Francisco have regained some excitement from buyers after a few months of slower gains — particularly among higher-priced homes — with monthly increases up by more than 5% from the month before.

The average monthly gains among low-tier homes accelerated in February, up 1.9%, though, again, that number is not seasonally adjusted. The high-tier monthly gains averaged 2.8% in February. The middle-tier monthly price increases averaged 2.4% (Figure 4).

With home price growth rising again and mortgage rates largely above the 5% psychological threshold, monthly expenses for most potential homebuyers are now much higher, up about 30% from a year ago. Nevertheless, demand for homes remains relatively high — or at least higher than before 2021. These buyers likely locked in more favorable mortgage rates in the early months of this year. However, the significant increase in rates seen since mid-March will be reflected in dampened demand going forward and in home sales numbers published in the early summer. As a result, overall home sales in 2022 could be lower than 2021, a reversal of previous forecasts, which called for higher home sales in 2022.

Nevertheless, it is interesting to note the strength in high-tier price segments, where buyer demand and purchasing power is less affected by changes in mortgage rates. The surge in monthly gains in markets such as Seattle, San Diego and San Francisco may reflect the focus on real estate investment as a hedge against inflation.