Mortgage Payments in 2021 Held Low by Low Interest Rates

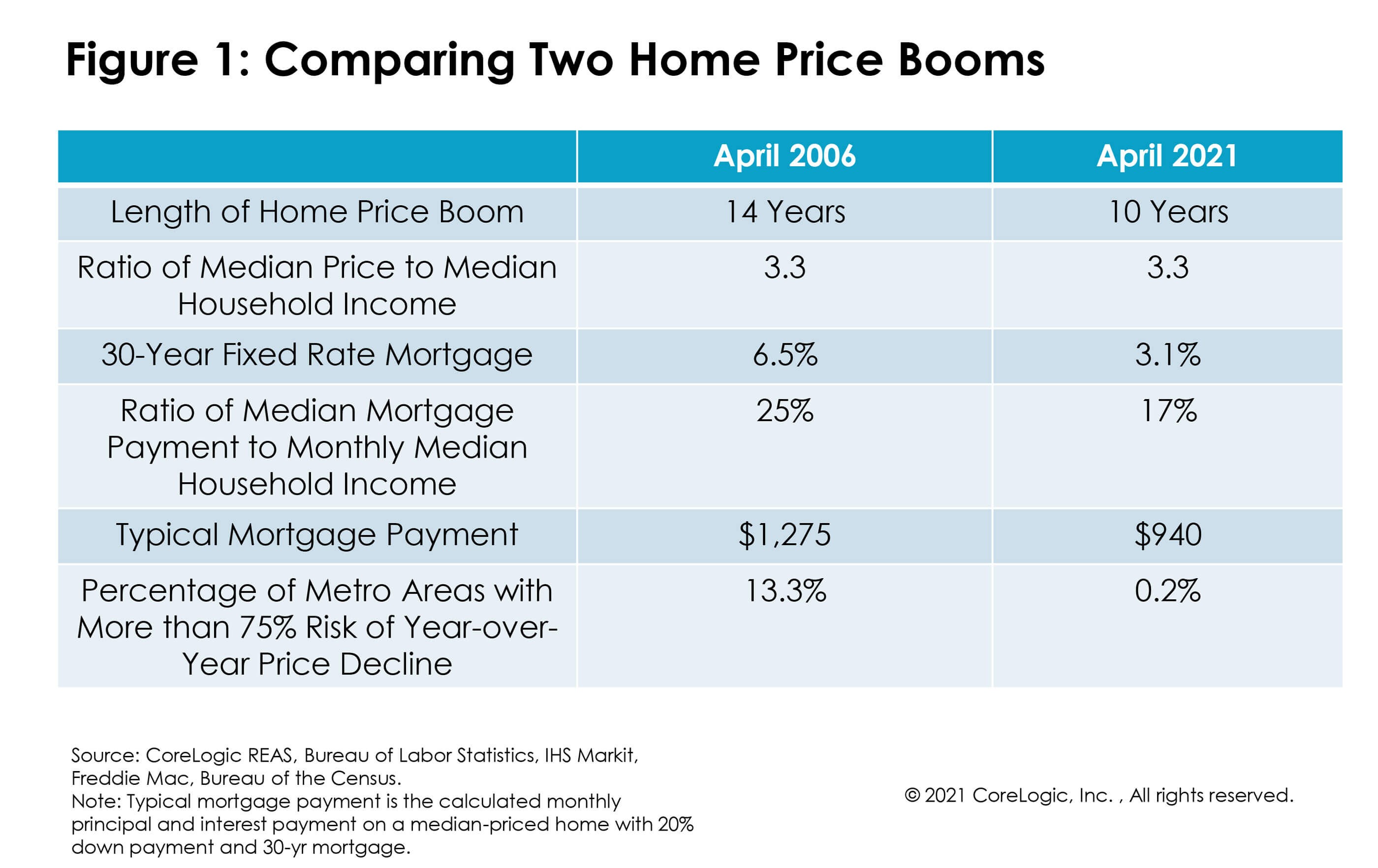

April 2021 marked the 15-year anniversary of the national home price bubble. In April 2006, home prices peaked just before heading to an unprecedented decline. As home prices soar in 2021, many comparisons are being made between the current housing environment and the one in 2006. However, despite recent double-digit home price appreciation, the mortgage payment to purchase a home is substantially more affordable than it was 15 years ago.

Home prices increased 13% in April 2021, which was the fastest year-over-year increase since February 2006. During the earlier housing market boom, home prices increased continuously for 14 years before reaching their peak in April 2006. The current housing market boom started in March 2011 and, so far, has lasted 10 years.

One similarity in the two periods is the ratio of median price to median income. In both April 2006 and April 2021, the median home price was about three times median household income.

One major difference between April 2006 and April 2021 is the level of mortgage interest rates. In 2006 the 30-year fixed rate mortgage rate was 6.5%, more than double the level in April 2021. Lower mortgage rates increase affordability by reducing the payment to income ratio — in 2006, a household spent 25% of their income on a mortgage payment, but in 2021, that ratio dropped to 17%.[1]

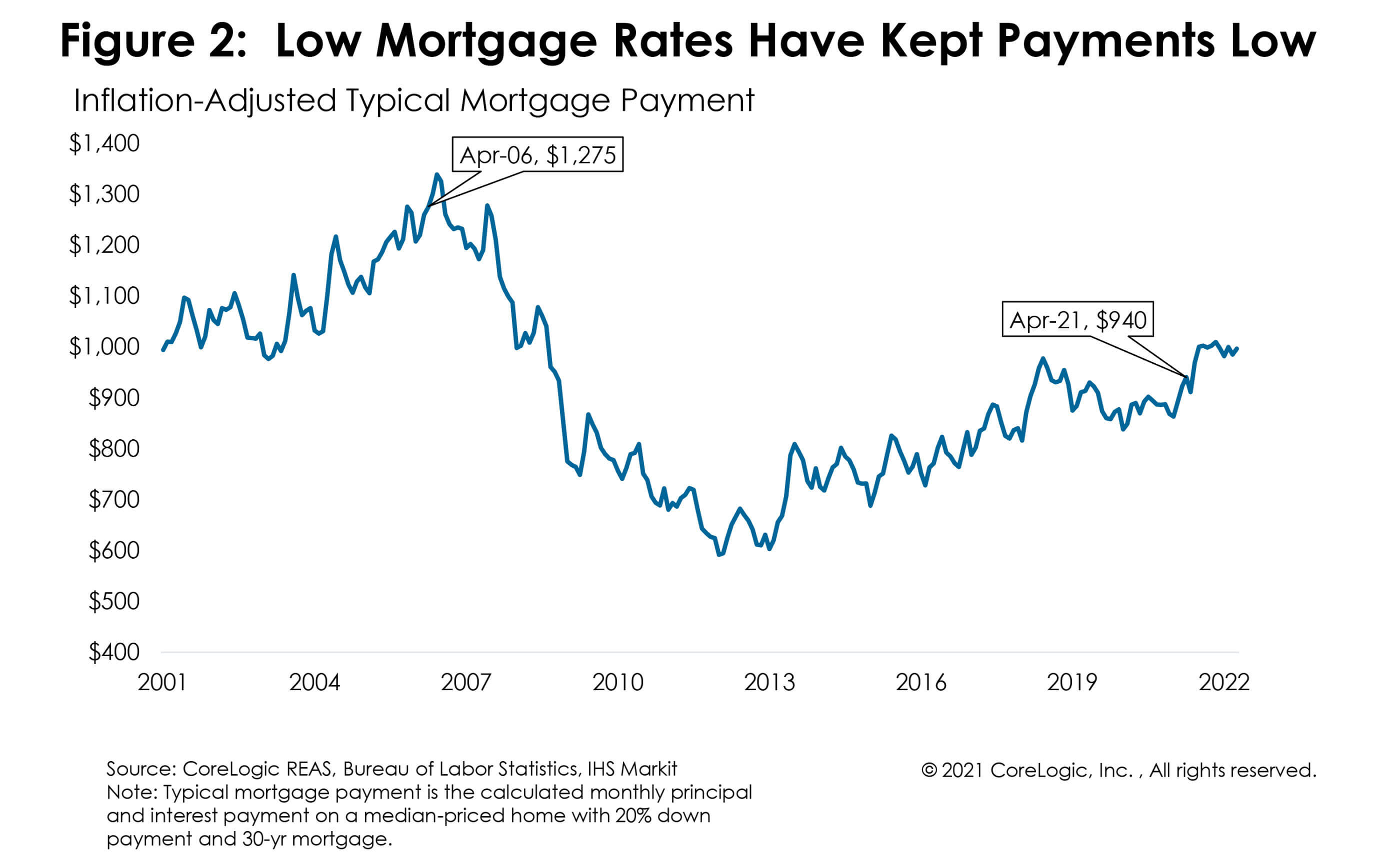

Put in other terms, the typical mortgage payment, which is the monthly payment a borrower would pay for a median priced home, was $1,275 in April 2006, but only $940 in April 2021. That’s a decrease of 26%.

Lower payment ratios significantly limit the risk of home price declines over the next 12 months. According to the CoreLogic Market Risk Indicators, 13% of metro areas were at risk for home price decrease in 2006, but that risk fell to near zero in 2021.

Home prices increased quickly so far in 2021, fueled by low inventory and low mortgage rates. As prices grow out of reach for some and inventory loosens, home price gains are expected to slow over the next year. However, rising interest rates will hurt affordability, with the typical mortgage payment projected to rise 6% to near $1,000 by April 2022.[2]

©2021 CoreLogic, Inc., All rights reserved.

[1] Mortgage payment is the calculated monthly principal and interest payment on a median-priced home with 20% down payment and 30-yr mortgage.

[2] Projected payment calculated using the HPI forecast increase of 2.8%, a fixed-rate mortgage increase to 3.5% and a 2% increase in the consumer price index.