Mother Nature can present a real threat to your business, as even a single event can cost billions of dollars in damages. What if you could understand a commercial property’s exposure to natural hazards in a single, automated workflow?

We help you more accurately identify and understand risk across a portfolio in a wide variety of high-peril areas—Water, Earth, Wind, Fire—to ensure accurate and timely coverage. We also offer a full suite of products that take the assessment of property claims risk for crime and non-weather water and fire to a whole new level. With easy-to-understand scores on a 100-point scale, you can more accurately assess the risk of individual policies.

From storm and fire hazards to land-based events such as sinkholes and earthquakes to crime risk, we’ve got you covered!

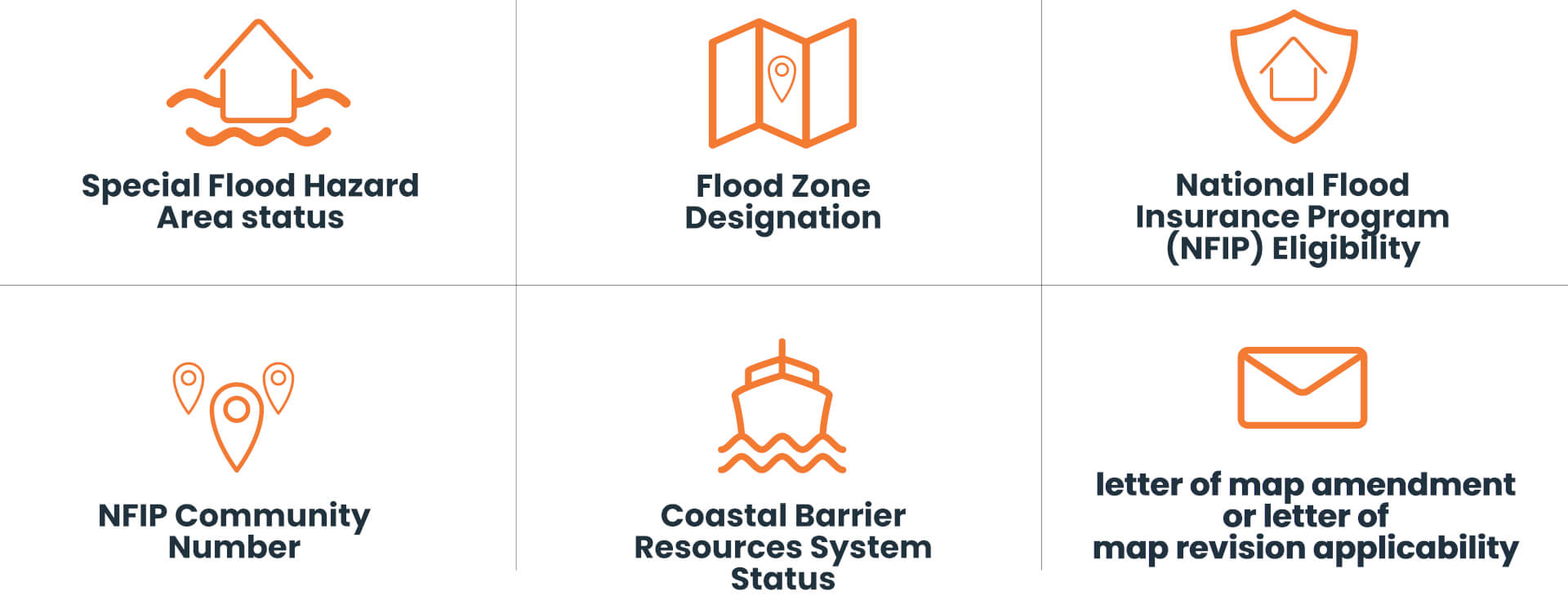

Water is a peril that is uniquely able to affect every location. Anticipating your water risk and predicting loss requires you to understand the details, like water flow and surrounding vegetation. Our models and scoring look at current and historical weather events, giving you the insight to take the guesswork out of knowing the condition of properties and the risk they face. Intelligence reports include:

According to the sigma study from Swiss Re, the United States has the most uninsured losses of any country. Underinsurance of natural catastrophe risk has risen steadily, and the majority of it involves earthquake risk. As insurers look to close the underinsurance gap, they need to pinpoint risk to establish more adequate premiums. Our intelligence reports include:

In 2018, over 1.7 million square miles saw severe (>60 mph) wind gusts in 2018, and 21,000 square miles saw very severe wind gusts (>80 mph).

Understanding the risk associated with thunderstorms, hurricanes, and severe convective storms which result in wind damage is essential to planning for it. CoreLogic’s granular wind data and ability to anticipate both loss and efficiently verify wind risk will bring you confidence in your portfolio. Intelligence reports include:

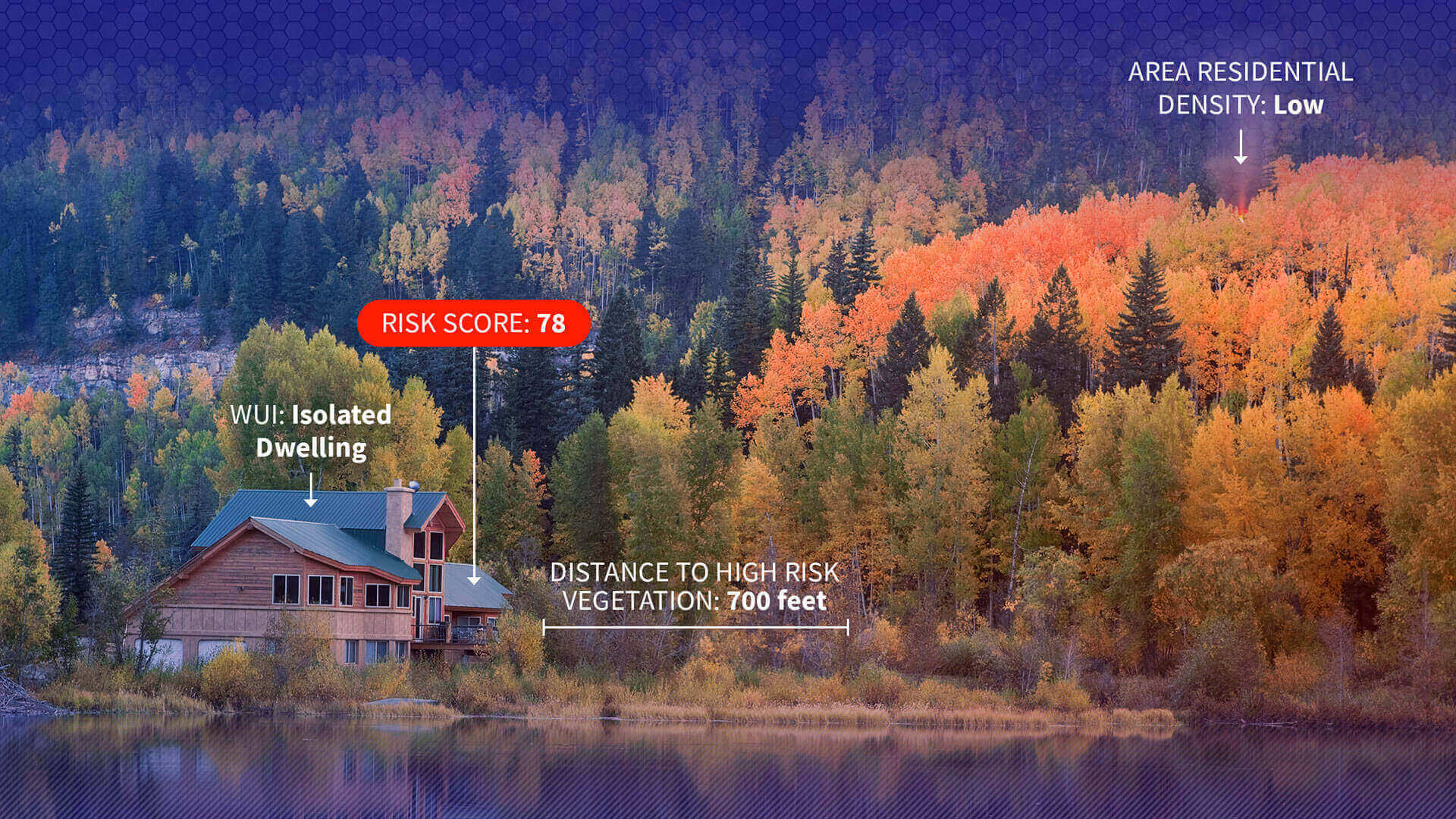

Fire hazards aren’t always the result of a natural occurrence. As our growing population continues to expand development, P&C portfolios are becoming more exposed to wildfire risk. Understanding fire-related risk requires an assessment of factors such as surface composition, surrounding vegetation and distance to the responding fire station. We help carriers pinpoint their fire hazard risk and establish better policy premiums without extensive on-site visits by utilizing the below intelligence:

Property insurers have historically been unable to accurately analyze the likelihood of non-weather hazards—such as plumbing and appliance leaks or the likelihood of house fires—due to a lack of consistent and complete data. Built from a broad, diverse and proprietary national database, our suite of products looks at the disparate causes of non-weather damage and their complex interactions to predict the probability of a claim and losses—for any address nationwide. Included intelligence reports are:

The past few years have been catastrophic, with everything from blazing wildfires to powerful hurricanes battering the coasts. We know clarity is important amidst the chaos, so we want to make sure you’re finding all the information you need to be up to date in one place.

At Hazard HQ™ you’ll find press releases, explanations of how our data works, commentary about what kind of damage we foresee, and critical thinking on what it takes to be more resilient in the face of natural hazards—be it a hurricane, volcano, earthquake, or beyond.

Help your team become everyday heroes by empowering your business with CoreLogic.